On May 18, 2026, the SBA announced something that sounds transformative: borrowers can now stack 7(a) and 504 loans for up to $10 million in combined federal financing. The press release called it “the highest level in agency history.”

The headlines wrote themselves. More capital. Bigger projects. A doubling of the previous $5 million cumulative cap.

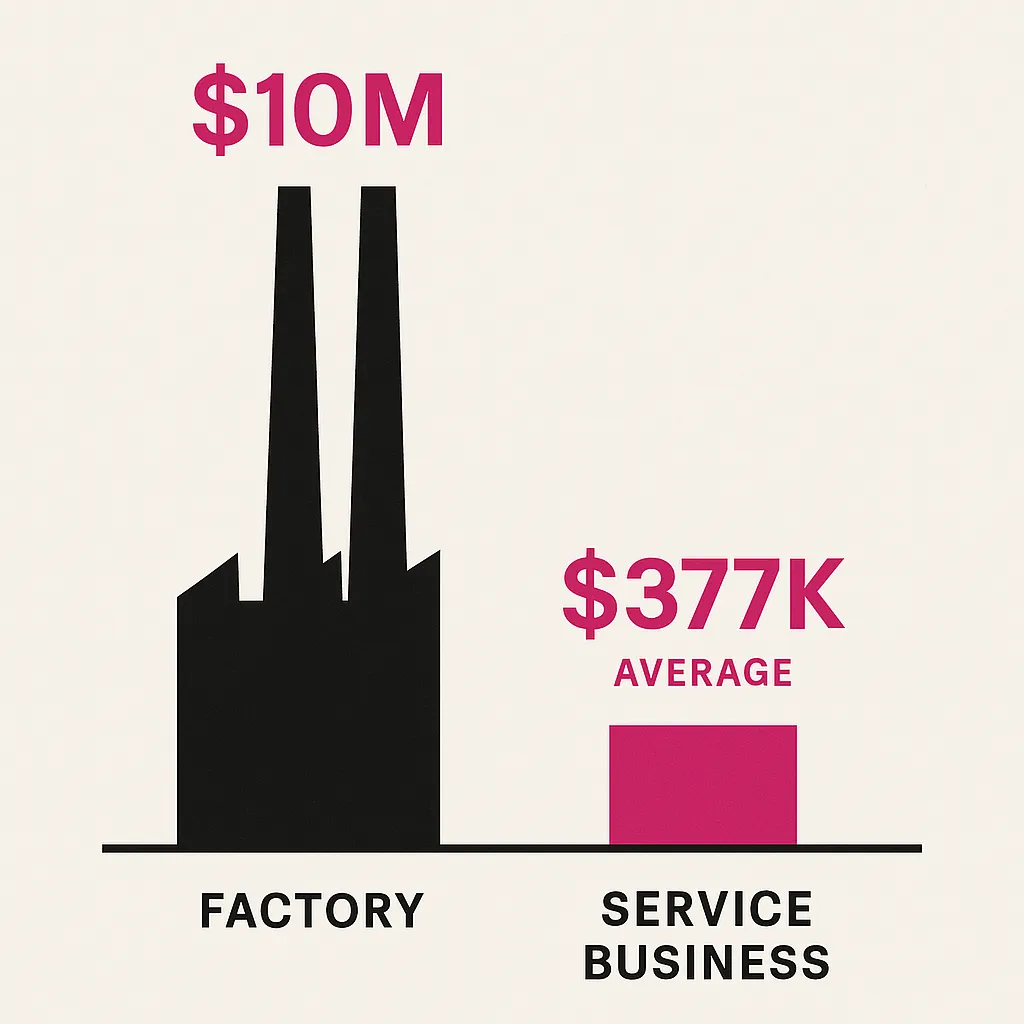

But here’s the number the headlines didn’t include: the average SBA loan to businesses with five or fewer employees is $377,192. Only 6.8% of SBA borrowers receive loans exceeding $2 million. The $10 million ceiling is structurally irrelevant to the vast majority of women-owned businesses.

This isn’t a coincidence. It’s a policy choice — and it reveals the SBA’s 2026 priorities with uncomfortable clarity.

The Manufacturing-First Agenda

The $10 million limit didn’t arrive alone. It’s one piece of a coordinated 2026 policy pivot toward manufacturing:

- Made in America Loan Guarantee (launched May 1): A 90% federal guarantee for manufacturers — compared to the standard 75% guarantee everyone else gets. That 15-point gap translates directly into lender willingness to approve.

- Waived loan fees for all manufacturers throughout FY2026. For a $1 million loan, that’s roughly $20,000–$26,000 in savings that service-sector borrowers still pay.

- $50 million Manufacturing E2G Grant Initiative (announced May 6): Direct grants for manufacturing workforce training and capacity building.

- 250+ manufacturer facility visits by SBA leadership across 25 states, plus 683 “Made in America” events reaching 11,000+ attendees.

Every dollar of new incentive, every fee waiver, every enhanced guarantee targets NAICS Sectors 31–33: manufacturing.

Where Women Aren’t

Women own approximately 39% of all U.S. businesses. But within manufacturing, that number drops to roughly 12%.

The sectors where women-owned businesses concentrate — professional services, healthcare and social assistance, other services (salons, pet care, consulting), retail, and education — received no new programs, no enhanced guarantees, and no fee waivers in the SBA’s 2026 agenda.

Here’s what that looks like in practice:

| SBA 2026 Policy | Manufacturing Borrower | Service-Sector Borrower |

|---|---|---|

| Maximum combined limit | $10M (effective July 4) | $10M (effective July 4) |

| Loan guarantee rate | 90% (Made in America) | 75% (standard) |

| Loan fees | Waived (FY2026) | Full fees apply |

| Dedicated grant programs | $50M E2G Initiative | None new |

| Dedicated SBA events | 683 events, 11,000+ attendees | None new |

The limit increase applies equally on paper. Everything else tilts the table.

The Qualification Wall

Even setting aside the sector tilt, the $10 million combined limit requires qualifications that screen out most women-owned businesses:

- Credit score of 700+ — the median credit score for women business owners applying for financing runs lower than for men, partly because women are more likely to be first-time borrowers

- Strong annual revenue — women-owned businesses generate 6% of all business revenue despite representing 39% of firms

- 2+ years operating history — women-owned businesses skew younger on average

- Significant collateral — women are less likely to own commercial real estate or other high-value assets that banks accept

The businesses that can actually stack $5 million in 7(a) with $5 million in 504 loans are established, capital-intensive, asset-heavy operations. The median woman-owned business requesting SBA financing asks for $40,000–$45,000.

The Real Gap Is at the Bottom, Not the Top

While the SBA celebrated its new $10 million ceiling, the gap that actually constrains women-owned businesses sits at the other end of the spectrum: the $50K–$150K funding dead zone where you’re too big for a microloan and too small to interest a bank.

- 54% of SBA microloans go to women-owned businesses — because microloans (average: $13,000) are one of the few programs that actually reaches them

- Just 19% of SBA 7(a) loans and 15% of 504 loans go to women-owned businesses

- Women are more likely to self-fund or avoid applying altogether — 56% of aspiring women founders plan to use personal savings

The SBA’s headline investment in 2026 is aimed at the top of the borrowing stack. The bottom — where women cluster — got the same programs it had before, minus the 43% workforce reduction at the SBA itself.

What This Actually Means for You

If you’re a woman business owner watching the $10M headline, here’s the honest read:

If you’re in manufacturing and have the revenue and collateral to qualify, this is genuinely good news. The 90% guarantee makes lenders significantly more willing to approve, and waived fees save real money. Apply through the SBA’s 7(a) program and ask your lender specifically about the Made in America Loan Guarantee.

If you’re not in manufacturing — and statistically, you’re probably not — here’s what moves the needle more than a loan limit you’ll never touch:

- CDFIs: Community Development Financial Institutions remain the most women-friendly lending channel, with programs specifically designed for underserved borrowers

- Alternative lenders: Women-owned businesses now represent 34% of funded applications in alternative lending networks, up from 28% in 2024. Algorithmic underwriting is showing near-perfect gender parity in approval rates

- Revenue-based financing: Now 22% of all small business lending applications, with repayment tied to revenue instead of fixed payments — structurally better for seasonal or growth-stage businesses

- SBA Microloans: If your capital need is under $50,000, the SBA Microloan program through intermediary lenders is still the most accessible SBA program for women

The Policy Question Nobody’s Asking

The SBA’s 2026 agenda isn’t wrong on its own terms. Manufacturing matters. Reshoring matters. The industries the Made in America Loan Guarantee targets employ millions.

But federal lending policy is a finite resource. Every dollar of enhanced guarantee capacity allocated to manufacturing is capacity not allocated to service businesses. Every fee waiver for manufacturers is revenue the SBA doesn’t collect — revenue that could fund Women’s Business Centers that are already losing staff.

The announcement mentioned construction, logistics, energy, and food production by name. It mentioned women-owned businesses zero times. That’s not an oversight. That’s a priority list — and you’re not on it.

The $10 million ceiling is real. For most women business owners, it’s also irrelevant. The question isn’t whether you can borrow more — it’s whether the system that’s supposed to help you is even looking in your direction.

Lendesca tracks SBA policy changes and helps small business owners navigate the shifting federal lending landscape — including identifying the programs that actually match your profile, not just the ones making headlines.