You know about the SBA rule changes. You’ve read about the citizenship lockout. You’ve tracked the WOSB scorecard shuffle.

Those are policy changes. You can plan around policy changes.

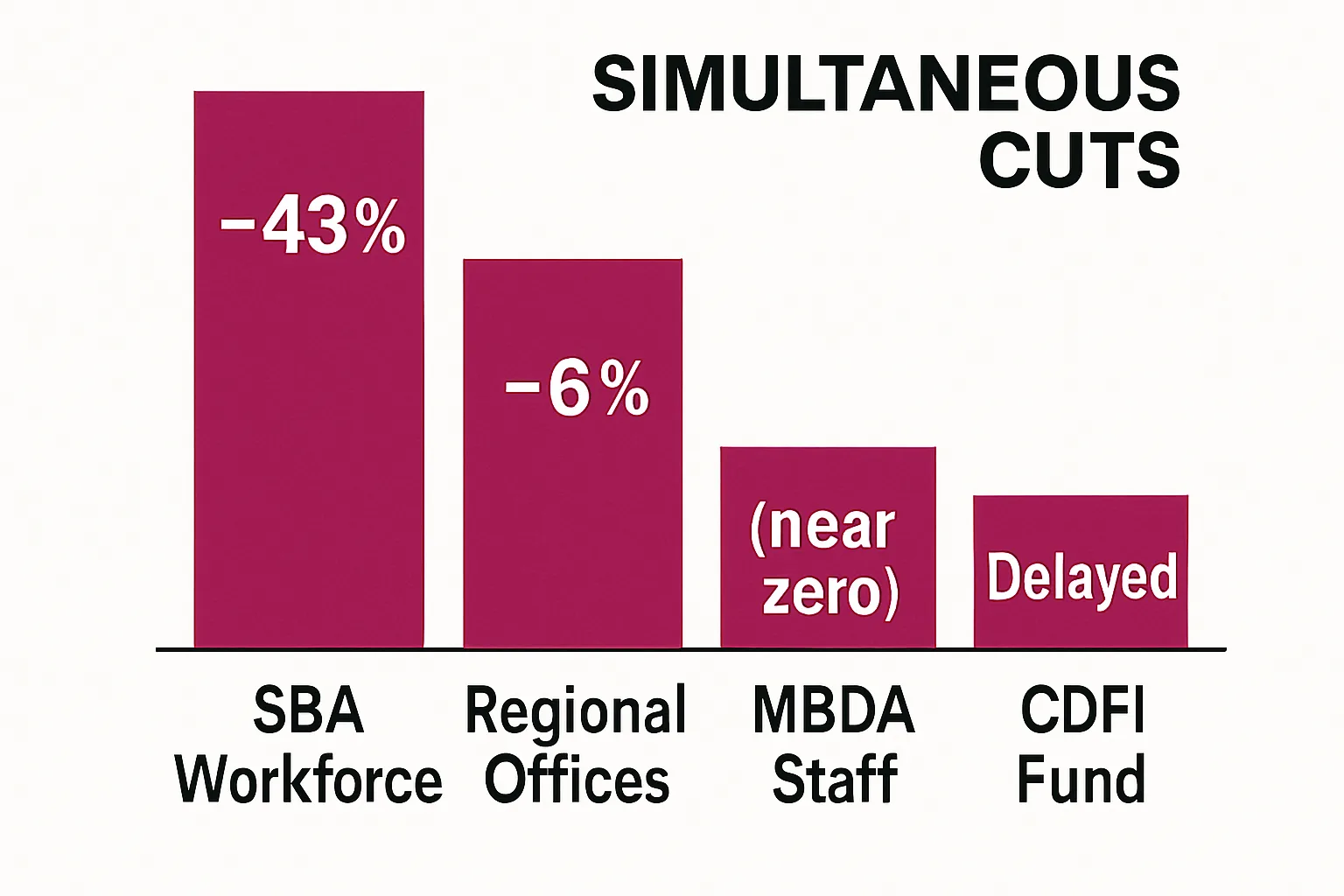

What you can’t plan around: the SBA just lost 43% of its workforce. And nobody is talking about what that means for the women who actually use the system.

What’s Been Lost

This isn’t about one program getting cut. It’s about the institutional infrastructure — the human layer between you and the bureaucracy — being dismantled simultaneously on multiple fronts.

SBA Workforce: Down 43%

The SBA’s workforce has been reduced by 43% since early 2025. Six regional offices have been relocated or consolidated. The people who processed loan applications, answered questions, ran workshops, and connected women with lenders? Many of them are gone.

What this means in practice:

- Longer processing times for SBA-guaranteed loans — fewer staff reviewing applications means longer queues

- Less outreach — district offices that used to run borrower education events and lender matchmaking have reduced capacity

- Fewer navigators — the people who helped first-time applicants understand which programs they qualified for are harder to reach

- More mistakes — when overworked staff process applications faster, errors increase, and errors in SBA applications mean delays or denials

MBDA: Operationally Dismantled

The Minority Business Development Agency — the only federal agency dedicated to supporting minority-owned businesses — has experienced sharp staffing declines. Its programs helped connect business owners with capital, contracts, and markets. Those services are functionally unavailable.

CDFI Fund: Delayed and Disrupted

The Treasury Department’s Community Development Financial Institutions Fund faces staff reductions, delayed fund disbursements, and administrative unpredictability. CDFIs are the lenders women turn to when banks say no — they use flexible underwriting, they lend in underserved communities, and they’re often the last stop before a woman gives up on funding entirely.

When the CDFI Fund’s capital deployment slows, the CDFIs themselves slow down. Fewer loans. Longer wait times. More conservative lending because their own funding is uncertain.

SBA Lending Standards: Tightened Simultaneously

The infrastructure collapse is hitting at the same time as underwriting is getting stricter:

- Streamlined loan cap reduced from $500,000 to $350,000

- Minimum business credit score increased from 155 to 165

- Mandatory equity injections reinstated for startups

- Lender discretion eliminated in favor of centralized SBA criteria

The streamlined process was designed to make smaller loans faster and easier. Cutting the cap from $500K to $350K means more borrowers get pushed into the full documentation process — which takes longer, requires more support, and is harder to navigate without help. And the help just got cut by 43%.

Why Women Feel This First

This isn’t just a budget story. It’s a gender story. Here’s why:

Women use institutional support more. The SBA’s Women’s Business Centers serve over 150,000 clients annually. Women are more likely to use WBCs, SCORE chapters, and district office resources than men — because the barriers they face require more navigation. When those resources shrink, the people who relied on them most are the people who lose the most.

Women apply for smaller loans. The SBA lending gap data shows women cluster in the loan sizes most affected by the streamlined cap reduction. More women were in the $350K–$500K streamlined range that now requires full documentation.

Women have less margin for error. When women receive the full requested loan amount only 37% of the time vs 51% for men, every additional barrier — a longer wait, a more complex form, a question that doesn’t get answered — compounds the disadvantage.

Women of color are hit hardest. Black women face 52–58% denial rates at traditional banks. Hispanic and Latina women face 45–50%. These are the women who most relied on CDFIs, WBCs, and SBA district offices as alternatives to a banking system that routinely rejects them.

What’s Still Standing

Not everything is gone. Knowing what’s still functional lets you focus your energy:

- Women’s Business Centers — Over 140 WBCs still operate. They’re strained but active. Find yours.

- SCORE — Free mentorship from retired business executives. Over 10,000 volunteer mentors. Not dependent on SBA staffing levels. Find a mentor.

- State and local programs — Many states have their own small business lending programs, grant funds, and technical assistance centers that are independently funded.

- CDFIs themselves — While the CDFI Fund is disrupted, individual CDFIs still operate with existing capital. The CDFI Locator can connect you with local options.

- Lendesca — For women navigating the lending landscape, Lendesca offers resources to help match borrowers with the right lending programs and understand what’s available.

How to Navigate a Shrinking System

Build your own navigation layer.

The system used to have guides. Now you need to be your own guide. Before applying for any SBA program:

- Research your specific loan program’s current processing times (they’ve changed)

- Identify 3–5 lenders who participate in the program, not just one

- Prepare complete documentation before your first conversation — you won’t get as many chances to go back and forth

- Build your business credit score before you need it — the minimum just went up

Find your people outside the system.

The best navigators now are other women who’ve recently been through the process. Join local women’s business networks, attend WBC events, and connect with women in similar industries who’ve successfully secured SBA financing in 2026. Their recent experience is more valuable than a government website that hasn’t been updated.

Apply wider, not harder.

With fewer SBA staff and tighter criteria, your odds at any single lender are lower. Compensate by applying to more lenders simultaneously. The non-bank funding map is a good starting point for understanding your full range of options.

Document the gaps.

If you can’t reach someone at a WBC, if your application sits for weeks without response, if you’re told a program exists but can’t find anyone to administer it — document it. This data matters for advocacy. Organizations like WIPP and the National Women’s Business Council need this evidence.

The Compound Effect

Individual policy changes are problems. Infrastructure collapse is a different category of threat.

When the SBA tightens underwriting and simultaneously cuts the staff who help borrowers meet those tighter standards, the two changes don’t add — they multiply. A harder application with less help isn’t twice as hard. It’s exponentially harder for the women who were already navigating the narrowest path to capital.

The safety net isn’t gone. But it’s thinner than it’s been in decades — and the SBA’s latest headline proves the pattern continues: see how the SBA’s $10M loan limit misses women-owned businesses. Meanwhile, the OBBBA introduced new ERC clawback risks for women business owners that compound the financial pressure. The women who get through will be the ones who stopped assuming the system would meet them halfway — and built their own infrastructure instead.