Here’s a number that should rearrange your entire borrowing strategy: women receive 47.7% less in loan amounts from traditional term lenders than men with comparable businesses.

From digital lenders? No gap. Zero. The same study — published in ScienceDirect and replicated across multiple research teams — found that when algorithms make the lending decision instead of humans, the gender disparity in initial loan amounts disappears.

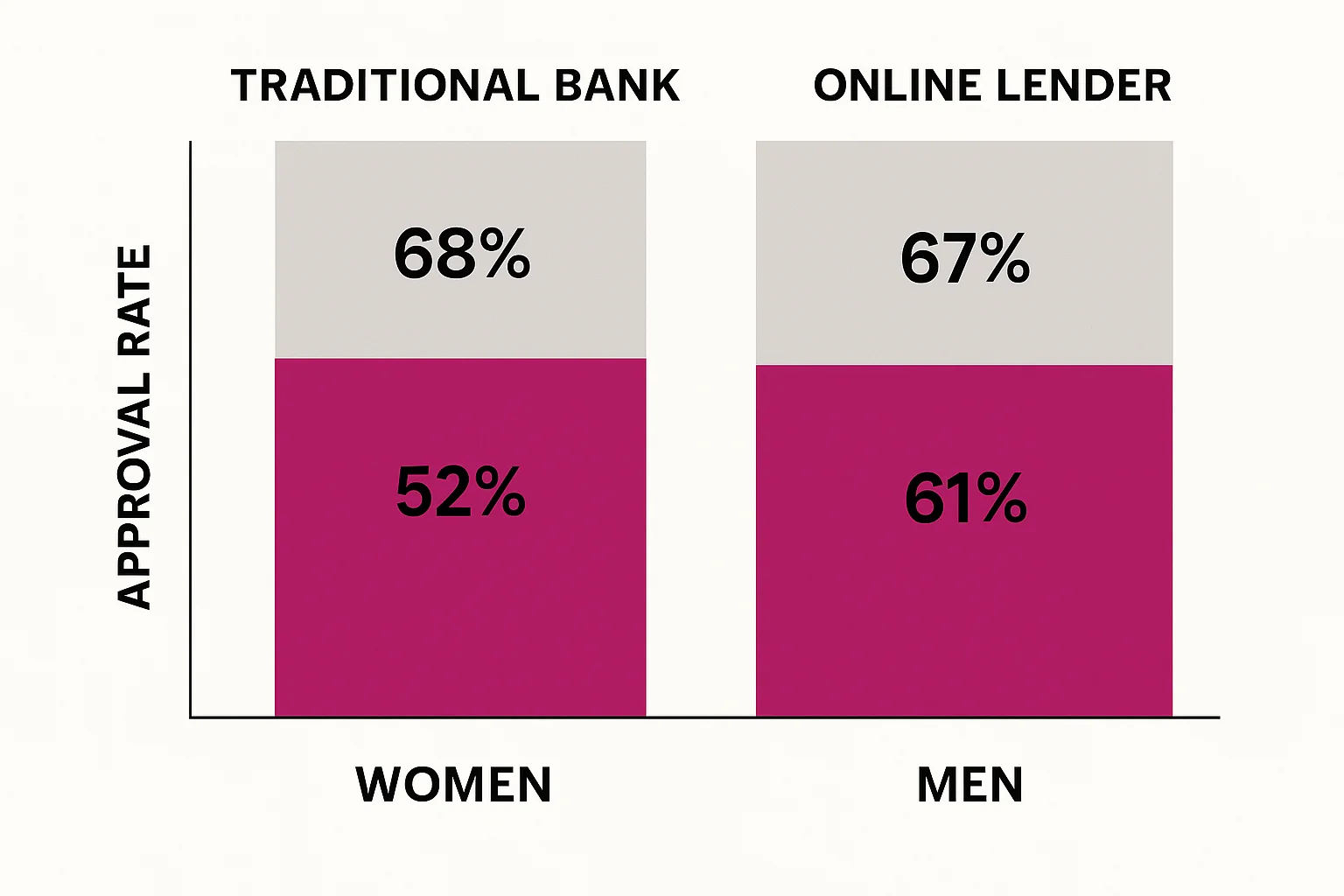

It gets sharper. Traditional bank approval rates: 52% for women vs. 68% for men — a 16-point canyon. Online lender approval rates: 61% vs. 67% — a 6-point gap that’s one-third the size.

The bias is in the banker. Not the borrower. When you remove the human from the decision, women’s businesses get funded at rates that reflect their actual creditworthiness.

So why are most women still walking into banks?

Why Algorithms Lend Differently Than Bankers

This isn’t about technology being inherently fair. Algorithms can perpetuate bias — that’s documented, and it’s real. But the specific biases that plague women’s business lending are disproportionately human biases that automated underwriting either doesn’t replicate or actively corrects for. A 2024 study in Nature Scientific Reports confirmed the pattern: fintech platforms structurally reduce the gender gap in lending outcomes.

What automated underwriting evaluates:

- Cash flow patterns — consistency, seasonality, trajectory

- Transaction velocity — how much money moves through your accounts and how frequently

- Revenue stability — recurring revenue, customer diversification, payment timing

- Digital footprint — online reviews, social presence, web traffic (yes, these factor into some models)

- Real-time business performance — not a snapshot from your last tax filing, but what’s happening right now

What automated underwriting doesn’t evaluate:

Your confidence level. Research shows investors and lenders ask men “promotion questions” (“How will you grow this business?”) and women “prevention questions” (“How will you prevent losses?”). Algorithms don’t ask questions at all.

Whether you “look like” a successful borrower. Pattern-matching to past successful borrowers is a core mechanism of human bias. If the mental model of a successful entrepreneur is a confident man in a suit, every woman starts at a disadvantage in a face-to-face meeting. Algorithms match to data patterns, not mental models.

How much you ask for. Women request 31–45% less in loan amounts than men — partly from discouraged borrowing, partly from conservative financial planning. Some fintech platforms set loan amounts based on what the data supports, not what you request — which can actually result in women being offered more than they’d have asked for.

The Fintech Lending Landscape: Who’s Actually Lending

Not all fintech lenders are created equal. Here’s the taxonomy that matters:

Revenue-Based Financing (RBF)

How it works: You receive capital and repay as a percentage of monthly revenue. High revenue month = higher payment. Slow month = lower payment.

Why it helps women: No collateral required. No personal guarantee in many cases. Approval based on revenue performance — and women-owned businesses generating consistent revenue qualify as readily as anyone.

Look at: Clearco, Pipe, Capchase (for SaaS/subscription businesses), Shopify Capital (for e-commerce)

The queue piece on revenue-based financing covers the broader alternative lending landscape.

Online Term Lenders

How it works: Fixed-term loans, typically 3–36 months, underwritten primarily on cash flow and bank transaction data.

Why it helps women: Decision in hours, not weeks. No relationship-building required — the algorithm doesn’t care that your banker doesn’t know your name. Approval rates significantly higher than traditional banks for comparable borrower profiles. (Though if you still value relationship-based evaluation, understand why the relationship lending alternative is disappearing.)

Look at: OnDeck, Funding Circle, Bluevine, National Funding

Invoice Financing

How it works: You advance against outstanding invoices. If your clients owe you money, you can access 80–90% of that value immediately.

Why it helps women: The credit decision is about your client’s ability to pay, not yours. If you invoice Fortune 500 companies, your gender and personal credit history are nearly irrelevant.

Look at: Fundbox, BlueVine, AltLINE

SBA-Facilitated Digital Lenders

How it works: Some online lenders offer SBA 7(a) loans with automated pre-qualification. You get the low SBA rates with the speed of fintech.

Why it helps women: Combines the best of both worlds — government-backed rates with reduced human bias in the initial screening. The SBA lending system still involves human decisions at final underwriting, but automated pre-qualification gets more women to that stage.

Look at: SmartBiz, Lendio (marketplace), Biz2Credit

What to watch for: higher interest rates as the tradeoff for accessibility — do the math on cost of capital vs cost of not having capital.

Building a Profile That Algorithms Love

Fintech underwriting evaluates you differently than a bank. Optimize accordingly.

Connect Your Business Bank Account

This is the single most important step. Fintech lenders pull 6–12 months of bank transaction data and evaluate:

- Average daily balance — consistency matters more than size

- Deposit frequency and sources — regular revenue from multiple customers signals stability

- Overdraft history — even one NSF in the past 90 days is a red flag in most models

- Expense patterns — steady, predictable expenses indicate an established operation

The fix: If your business finances are intermingled with personal accounts, separate them now. Clean cash flow in a dedicated business account is the foundation of algorithmic approval.

Maximize Digital Revenue Signals

Algorithms love data they can verify independently:

- Online sales through payment processors — Stripe, Square, PayPal all create auditable transaction histories

- Recurring subscriptions or retainers — recurring revenue is the strongest signal in most models

- Digital invoicing — invoices sent through platforms (QuickBooks, FreshBooks) create records algorithms can read

- E-commerce platform data — Shopify, Amazon, Etsy sales histories are high-signal for relevant lenders

Meet the Thresholds

Most fintech lenders have minimum requirements:

- Time in business: 6–12 months minimum (some accept 3 months for marketplace models)

- Annual revenue: $50K–$100K minimum for most term lenders; $25K+ for some marketplace and RBF products

- Personal credit score: Varies widely — some platforms lend to 500+ FICO, others want 600+

- No recent bankruptcies: Usually 1–2 year lookback

Build the Reporting Trail

Some fintech lenders report to business credit bureaus — Dun & Bradstreet, Experian Business, Equifax Business. Successful repayment on a fintech loan can build your business credit profile, which strengthens future applications to both fintech and traditional lenders.

Ask before you borrow: “Do you report to business credit bureaus?” If yes, this loan does double duty — it’s capital and credit-building.

When Traditional Banking Still Wins

Fintech isn’t the answer to everything. Be strategic about when to use which channel.

SBA 7(a) and 504 loans — If you qualify, these are still the cheapest money in small business lending. Rates of 7–10% vs. fintech rates of 15–45%. For large, long-term needs (equipment, real estate, major expansion), the rate difference compounds dramatically. Worth the slower process and relationship requirements.

Commercial real estate — Still heavily relationship-dependent. Automated underwriting hasn’t cracked CRE lending at scale. If you’re buying property, you need a banker.

Very large loans ($500K+) — Most fintech platforms cap between $250K–$500K. For larger capital needs, traditional lending provides scale that fintech can’t match.

The hybrid strategy that works: Use fintech for speed and first capital. Build a repayment track record. Then approach traditional lenders with 12–24 months of performance data. You’re no longer asking to be trusted — you’re showing receipts. The non-bank funding map covers how these channels work together.

The Red Flags: What Fintech Lending Can Cost You

Accessibility comes at a price. Eyes open.

Higher APRs

This is the big one. Fintech convenience typically costs:

- Online term loans: 15–45% APR (vs. 7–13% for SBA/bank loans)

- Revenue-based financing: Factor rates of 1.1–1.5x (which can translate to 20–80% APR depending on repayment speed)

- Invoice financing: 1–5% per month on the advanced amount

- Merchant cash advances: Effective APRs of 40–350% — avoid these. The credit card capital trap covers why expensive capital becomes a cycle.

Run the numbers. A $50K loan at 30% APR costs $15K per year in interest. The same loan at 8% through SBA costs $4K. If you can wait 60–90 days for SBA approval, you save $11K. If you can’t wait — because the opportunity disappears or the cash flow crisis is now — fintech is the rational choice. But know the cost.

Daily or Weekly Repayment

Some platforms pull repayment daily from your bank account. This smooths their risk but hammers your cash flow. A $500/day draw is $10K/month leaving your account automatically. Make sure your cash flow modeling accounts for this.

Stacking Risk

Easy approval means easy over-borrowing. It’s possible to have three fintech loans running simultaneously — and each one’s daily draw competing for the same cash flow. This is how businesses that could have survived with one well-sized loan spiral into debt that becomes unmanageable.

Rule: one fintech loan at a time unless you’ve stress-tested the combined payment against your worst-month revenue.

Data Privacy

You’re giving lenders deep access to your business bank account, accounting software, and payment processors. Understand what you’re sharing, how long they retain it, and whether they sell aggregated data. Read the data-sharing agreement. Actually read it.

The Bottom Line

The gender gap in business lending is a human problem. The Federal Reserve’s Small Business Credit Survey confirms it year after year: when humans make the decision, women get less. When algorithms make the decision, the gap shrinks to near-zero.

This doesn’t mean fintech is always the right choice. It means your lending strategy should account for where the bias lives — and route around it when the math works.

If you’ve been denied by a traditional bank, the denial may say more about the bank than about your business. Before you accept that verdict, test it against a lender that evaluates your data instead of your demeanor.

The algorithm doesn’t care about your gender. It cares about your cash flow. Make sure your cash flow tells a clear story — then let the numbers speak.

Explore the full map of non-bank funding options available to women business owners.