The Problem Nobody Talks About

You took three months off to have a baby. During that time, your revenue dropped 40-60%. Maybe you closed entirely for six weeks. Maybe you kept the lights on but operated at half capacity.

Now it’s 18 months later. You need a $75,000 loan to expand. You pull together two years of tax returns, like every lender requires.

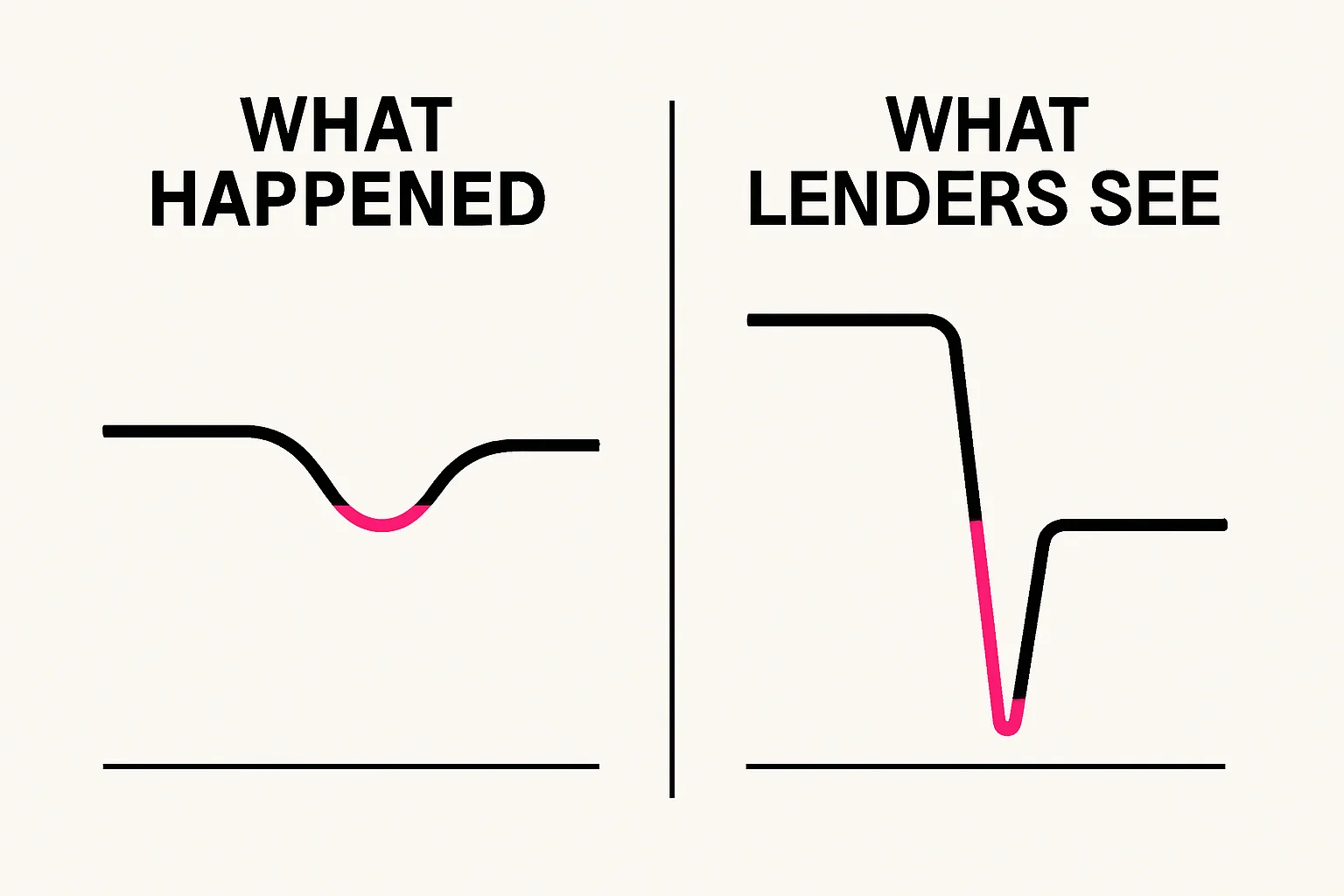

Year one shows strong, growing revenue. Year two shows a crater — followed by recovery, but the annual total is still 30% below the prior year.

The loan officer doesn’t see a woman who built a business, had a child, and came back stronger. The loan officer sees a business that declined.

There is no field on an SBA loan application for “I had a baby.” There is no way to mark a quarter as “parental leave” on a Schedule C. The lending system was not designed for people whose bodies create human beings.

The Numbers Behind the Penalty

Here’s what the data actually shows:

- 37% of women business owners who need financing don’t apply because they expect rejection — a rate 42% higher than men (26%), according to the Federal Reserve’s Small Business Credit Survey

- Self-employed women receive zero paid leave in 36 states — meaning time off equals zero revenue, not reduced revenue

- Lenders evaluate 2-3 years of financials as standard underwriting — a pregnancy that happened 18 months ago is still in the evaluation window

- Revenue consistency matters more than revenue size for many lenders — a dip-and-recovery pattern triggers more scrutiny than steady lower revenue

The cruelest part: women who’ve had children and maintained their businesses demonstrate exactly the resilience and operational capability lenders claim to value. But the algorithm doesn’t measure resilience. It measures trend lines.

How the System Fails

The Tax Return Problem

Your Schedule C or business tax return reports annual totals. A year in which you earned $180,000 in nine active months looks identical to a year in which you earned $180,000 across twelve mediocre months. But a year in which you earned $135,000 because you took three months off — that looks like decline from a prior year of $180,000.

Lenders don’t read your return and ask “why?” They calculate year-over-year change and assign risk scores.

The Bank Statement Problem

SBA lenders increasingly use 12-24 months of bank statements alongside tax returns. A three-month gap with minimal deposits followed by rapid recovery doesn’t read as “maternity leave” — it reads as “seasonal business with irregular cash flow” or worse, “business that nearly failed.”

The Credit Utilization Problem

Many women increase personal credit card usage during maternity leave to cover household expenses their business income normally covers. This temporarily spikes credit utilization — one of the heaviest-weighted credit score factors — creating a one-two punch: lower business revenue AND lower personal credit score, hitting right when you’re most likely to need business financing for the restart.

Who Gets Hit Hardest

Not every self-employed woman experiences this equally:

- Solo practitioners and solopreneurs — no team to maintain revenue during absence

- Service-based businesses — revenue stops when the service provider stops (vs. product businesses that can ship inventory)

- Cash-based businesses — no contracts or recurring revenue to show “the business continued, I just stepped back”

- Women in states without paid leave — 36 states offer nothing for self-employed workers, according to the Bipartisan Policy Center’s state leave tracker

- Women who’ve had multiple children within the evaluation window — two dips in three years looks like a structurally failing business

What You Can Do: The Documentation Strategy

The lending system won’t change quickly. But you can change how your story is told within it.

Before Maternity Leave

Build your paper trail proactively:

- Write a formal business continuity memo — date-stamped, filed in your business records. State that you’re taking parental leave from [date] to [date] and outline your return plan. This becomes evidence in future loan applications.

- Maintain minimum business activity — even one invoice per month during leave keeps your bank statements from showing a complete gap. A $500 retainer client is worth more than $5,000 in lost lending credibility.

- Separate leave expenses from business expenses — don’t run personal maternity costs through business accounts. Clean financial separation makes the “business pause” visible as a pause, not a failure.

- Pre-build your business credit profile — PAYDEX scores and business credit reports can continue building during leave if you have vendor accounts with auto-pay.

After Maternity Leave

Rebuild the narrative in your financials:

- Create a revenue addendum — a one-page document that explains the revenue pattern. Include: pre-leave trailing 12-month revenue, the leave dates, post-leave trailing revenue showing recovery trajectory. Many SBA lenders accept addendums with applications.

- Use the right comparison period — instead of year-over-year tax returns showing decline, present trailing-6-month financials showing your post-return growth rate. Many non-bank lenders weight recent performance over annual totals.

- Get a CPA letter — a brief letter from your accountant confirming that the revenue variation corresponds to a documented parental leave period adds professional credibility to your addendum.

- Time your application strategically — if possible, wait until your post-return revenue creates a full 12-month trailing period that shows strong performance. Applying at month 8 of your return when you only have 8 months of strong data means you’re voluntarily showing the gap.

Choosing the Right Lender

Not all lenders evaluate the same way:

- CDFIs — Community Development Financial Institutions are designed to evaluate borrowers holistically. Many have experience with the maternity gap and can account for it in underwriting.

- Revenue-based lenders — evaluate current revenue, not historical tax returns. If your post-return revenue is strong, the history becomes less relevant.

- SBA microloan intermediaries — smaller loan amounts with more flexible underwriting. The SBA microloan program goes to women 46.5% of the time precisely because these intermediaries look at the full picture. See our SBA loan playbook for the full breakdown.

- Lenders with female loan officers — research from the ECB Working Paper Series shows female loan officers are significantly more likely to correctly evaluate female borrowers’ risk profiles.

The Policy Gap

This problem has a structural solution: any lender could add a “documented leave of absence” field to their underwriting evaluation. Just as disability leave doesn’t automatically disqualify borrowers in mortgage lending, parental leave shouldn’t automatically code as risk in business lending.

Until that changes:

- 14 states + DC now offer paid family leave programs, many with self-employed opt-in options. Washington, Colorado, Connecticut, Massachusetts, and Oregon have been live. Delaware and Minnesota launched January 2026.

- The IRS Section 45S tax credit gives employers a tax credit for paying employees during leave — but nothing equivalent exists for self-employed individuals paying themselves.

The systemic fix requires either lender policy changes or regulatory guidance distinguishing documented parental leave from business decline. Neither is imminent. In the meantime, documentation and lender selection are your strongest tools.

The Bigger Picture

The discouragement rate — 37% of women who need funding not applying because they expect rejection — is almost certainly higher among women with maternity-related revenue gaps. They KNOW their financials look weak. They KNOW lenders won’t understand. So they don’t apply, and the capital gap widens.

This isn’t about whether women should take time off to have children. It’s about whether the lending system can distinguish between a business that’s failing and a business whose owner did something fundamentally human — and came back.

Your revenue dip isn’t a red flag. It’s a story about building something bigger than your business. The system just doesn’t know how to read it yet.