You’ve been told the problem a hundred times: lenders want collateral. Real estate. Equipment. Inventory you can photograph and appraise. And if you don’t have those things — or enough of those things — you’re signing a personal guarantee that puts your family’s assets on the line.

But here’s what nobody told you: your brand name is collateral. Your proprietary recipe is collateral. Your original designs, your software, your content library — all collateral.

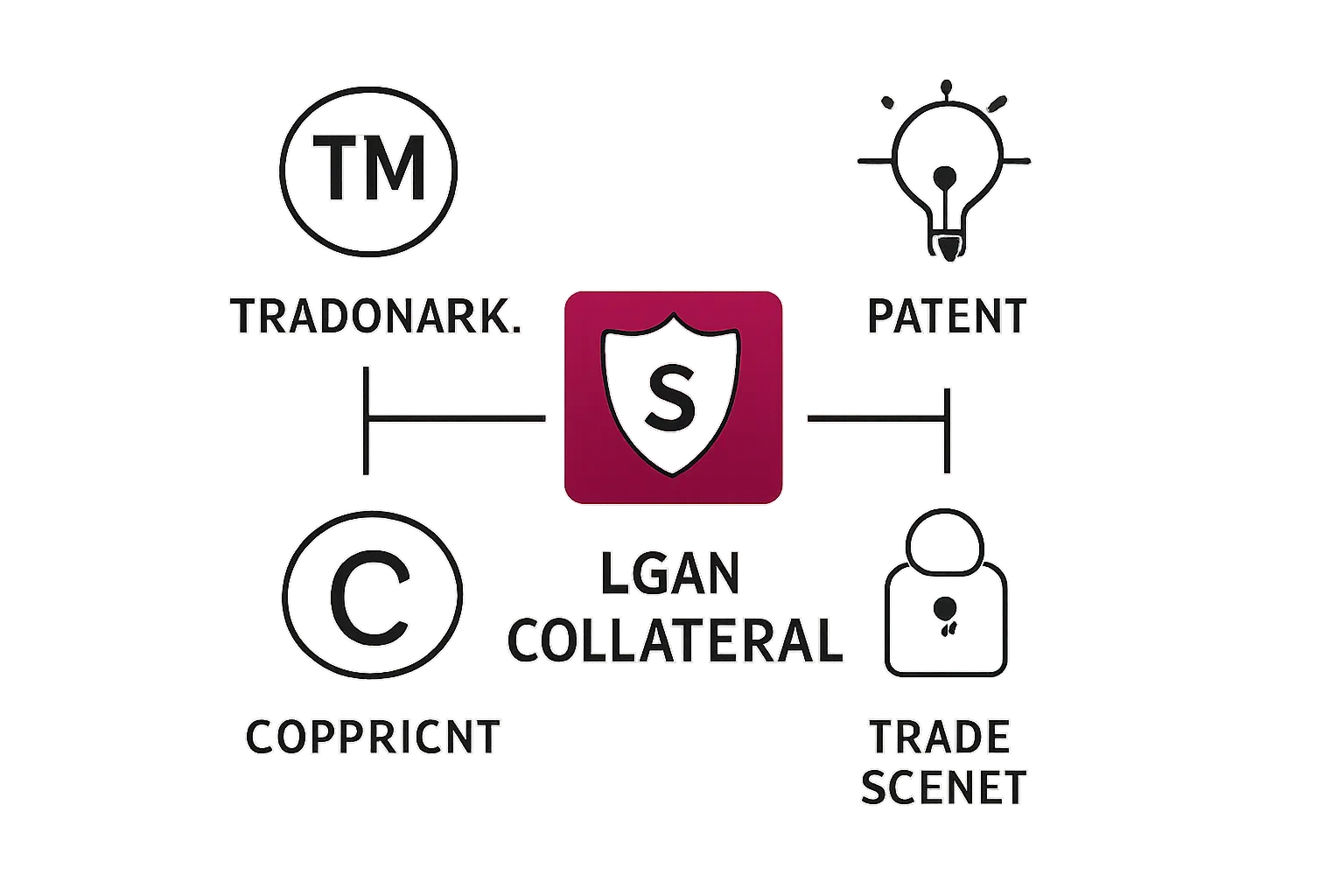

Intellectual property — trademarks, patents, copyrights, trade secrets — is a legitimate, lendable asset class. Firms with registered IP show 38% lower probability of default and 50% lower losses when things go wrong. Startups are 2.5x more likely to secure seed funding after filing a trademark. And SBA lenders can accept IP as collateral on government-backed loans.

Women own 42% of U.S. businesses. Women dominate creative industries — fashion, beauty, food, crafts, design, content — where trademarks and copyrights are the primary IP. Yet only 10.9% of U.S. patent inventors are women, which means the entire IP-as-collateral conversation has been framed around patents and tech — the forms of IP where women are least represented.

That framing is wrong. And it’s costing you money.

The Numbers That Should Change How You Think About IP

The data here isn’t ambiguous. It’s directional and it’s large:

- 38% lower default rate. A UK IPO/British Business Bank study analyzing over 20,000 loans found that firms with registered IP were significantly less likely to default — and when they did, losses were 50% lower than peers without IP.

- 2.5x more likely to get funded. Research on startup financing shows that filing a trademark more than doubles your odds of securing seed-stage capital. Filing a patent makes you 2.9x more likely.

- Personal guarantee elimination. IP collateral can replace or reduce the personal guarantee requirement — because lenders already have a claim on something valuable. This directly addresses the personal guarantee trap that disproportionately affects women borrowers.

- SBA accepts it. SBA lenders can and do take security interests in intellectual property. This isn’t a niche fintech product — it works within the government-backed lending infrastructure women already use.

What makes this especially relevant for women: the collateral gap is one of the most documented barriers in women’s business lending. Women request 31–45% smaller loan amounts than men, partly because they have less traditional collateral to pledge. IP doesn’t close that gap entirely — but it adds an asset class that most women already own and nobody’s told them counts.

How IP-Backed Lending Actually Works

Here’s the process, stripped of jargon:

1. Identify Your IP Assets

Before you talk to a lender, inventory what you own:

- Trademarks: Your business name, logo, product names, taglines — anything that identifies your brand in the marketplace

- Copyrights: Original content, designs, photography, software code, educational materials, course content

- Patents: Inventions, processes, formulas, unique methods (provisional patents count as signal, too)

- Trade secrets: Proprietary processes, customer databases, supplier relationships documented in operating procedures

2. Get a Valuation

IP valuation typically uses one of three approaches:

- Income approach: How much revenue does this IP generate or contribute to? (Most common for lending)

- Market approach: What have similar IP assets sold for?

- Cost approach: What would it cost to recreate this IP from scratch?

For lending purposes, the income approach dominates. A trademark attached to a business generating $500K in annual revenue has a demonstrable value — the brand is part of why customers buy.

3. Perfect the Security Interest

This is the legal step that makes IP function as collateral:

- Patents and trademarks: File a UCC-1 financing statement and record the security interest with the USPTO

- Copyrights: Record with the U.S. Copyright Office

- Trade secrets: Documented in the loan agreement with confidentiality protections

4. Negotiate the Terms

Typical IP-backed loan terms:

- Loan-to-value: Usually 20–50% of the qualified IP value

- Interest rates: Comparable to other asset-backed lending — your IP is just another form of collateral

- NatWest example: In 2024, NatWest launched the first mass-market IP-backed lending product — loans from £250K to £10M at up to 50% of qualified IP value. The U.S. market is following.

Your IP Inventory: A 15-Minute Audit

Grab a pen. This takes less time than your last coffee run.

Brand Assets (Trademark Territory)

- Business name — registered? If not, is it registrable?

- Logo — registered?

- Product or service names — any distinctive enough to trademark?

- Taglines or slogans you use consistently

Creative Assets (Copyright Territory)

- Original website content, blog posts, or guides

- Course materials, training content, or educational programs

- Photography, illustrations, or design assets you created

- Software, apps, or digital tools you built

- Books, e-books, or published materials

Innovation Assets (Patent Territory)

- Proprietary processes or methods

- Unique formulas or recipes

- Technical inventions or product innovations

- Systems you built that solve a specific problem differently

Operational Assets (Trade Secret Territory)

- Customer databases and relationship records

- Supplier agreements and sourcing methods

- Pricing models or financial methodologies

- Internal processes documented in SOPs

What’s most valuable to lenders (ranked):

- Established trademarks with revenue history

- Patents with commercial application

- Copyrights generating licensing revenue

- Trade secrets with documented competitive value

What it costs to register:

- Trademark: ~$250–$350 per class (USPTO filing), plus attorney fees of $500–$2,000

- Copyright: ~$65 (single work, online filing)

- Provisional patent: ~$1,600–$3,000 (buys 12 months to file a full patent)

Making the Case to Your Lender

Most lenders won’t ask about your IP. You need to bring it up.

What to prepare:

- A one-page IP inventory listing each asset, its registration status, and its role in revenue generation

- Revenue attribution — what percentage of your business’s value depends on brand recognition, proprietary content, or protected processes?

- Any licensing revenue or potential licensing revenue from your IP

- Registration certificates or application receipts

How to frame it:

Don’t say “I have some trademarks.” Say: “My registered trademark has been associated with $400K in annual revenue for three years. I’d like to discuss including it as supplementary collateral.”

Even when IP isn’t your primary collateral, raising it signals business maturity. It tells the lender you think about your business as an asset portfolio — exactly the mindset they want to see in a borrower.

Where to look for IP-savvy lenders:

- SBA Preferred Lenders with experience in service or creative industry businesses

- Non-bank funding sources including specialized asset-based lenders

- CDFIs that serve creative economy businesses

- Platforms like Lendesca that help women navigate lending options across traditional and alternative channels

- The USPTO’s Women’s Entrepreneurship (WE) program for mentorship on leveraging IP

Protect It Before You Pledge It

IP you haven’t registered is harder to use as collateral and worth less in every lending conversation you’ll ever have.

The registration-to-fundability pipeline:

Register your most valuable IP now — even if you’re not borrowing for another year. Registration creates a public record of ownership, establishes priority dates, and makes valuation straightforward. It’s building business credit for your intangible assets.

Common mistakes that erode IP value:

- Not separating personal and business IP. If your business uses a trademark registered in your personal name, lenders see a mess. Register under the business entity.

- Failing to document ownership in partnerships. If you co-founded the business, who owns the brand? The logo? The proprietary process? Get this in your operating agreement before it becomes a lending issue.

- Letting registrations lapse. Trademark registrations require maintenance filings. A lapsed registration is worth less than an active one.

- Not enforcing your rights. IP you don’t protect can lose its legal status — especially trademarks. If competitors use your brand name and you don’t act, you’re diluting your own collateral.

The Bottom Line

You’ve been playing the collateral game with one hand behind your back. Every brand you built, every original process you developed, every piece of content you created — those are assets. They have value. And that value can be pledged.

The IP-to-funding pipeline is especially powerful for women because it doesn’t require the traditional assets that the wealth gap makes harder to accumulate. You don’t need to own commercial real estate to have collateral. You just need to own — and register — what you’ve already built.

Start with the 15-minute audit. Register what’s registrable. And the next time a lender asks what you can pledge, hand them a list that includes your brain.