Every SBA loan in America requires a personal guarantee from anyone who owns 20% or more of the business. That’s the rule. It doesn’t change based on your marital status, household structure, or personal net worth.

But the impact of that rule is wildly unequal.

A married founder with joint home equity, a spouse’s retirement account, and family property can pledge $400K in collateral without touching their business. A single founder whose primary asset is the business itself faces a math problem that no amount of financial literacy can solve: the thing securing the loan is the thing the loan funds.

Women receive the full amount they request only 37% of the time, compared to 51% for men. Partial approvals — “we’ll give you $200K of the $350K you asked for” — correlate strongly with insufficient collateral coverage. This isn’t a credit score problem. It’s a structural wealth problem wearing a policy-neutral mask.

The Math Problem Nobody Names

The SBA 7(a) program — the most common business acquisition and growth loan in America — requires:

- Personal guarantee from all owners with 20%+ stake

- All available collateral pledged (business AND personal)

- No defined minimum collateral-to-loan ratio (but lenders have their own)

In practice, lenders want to see guarantee coverage — pledged assets relative to loan amount — of at least 1:1. Many prefer 1.5:1 or higher.

Here’s where the asymmetry bites:

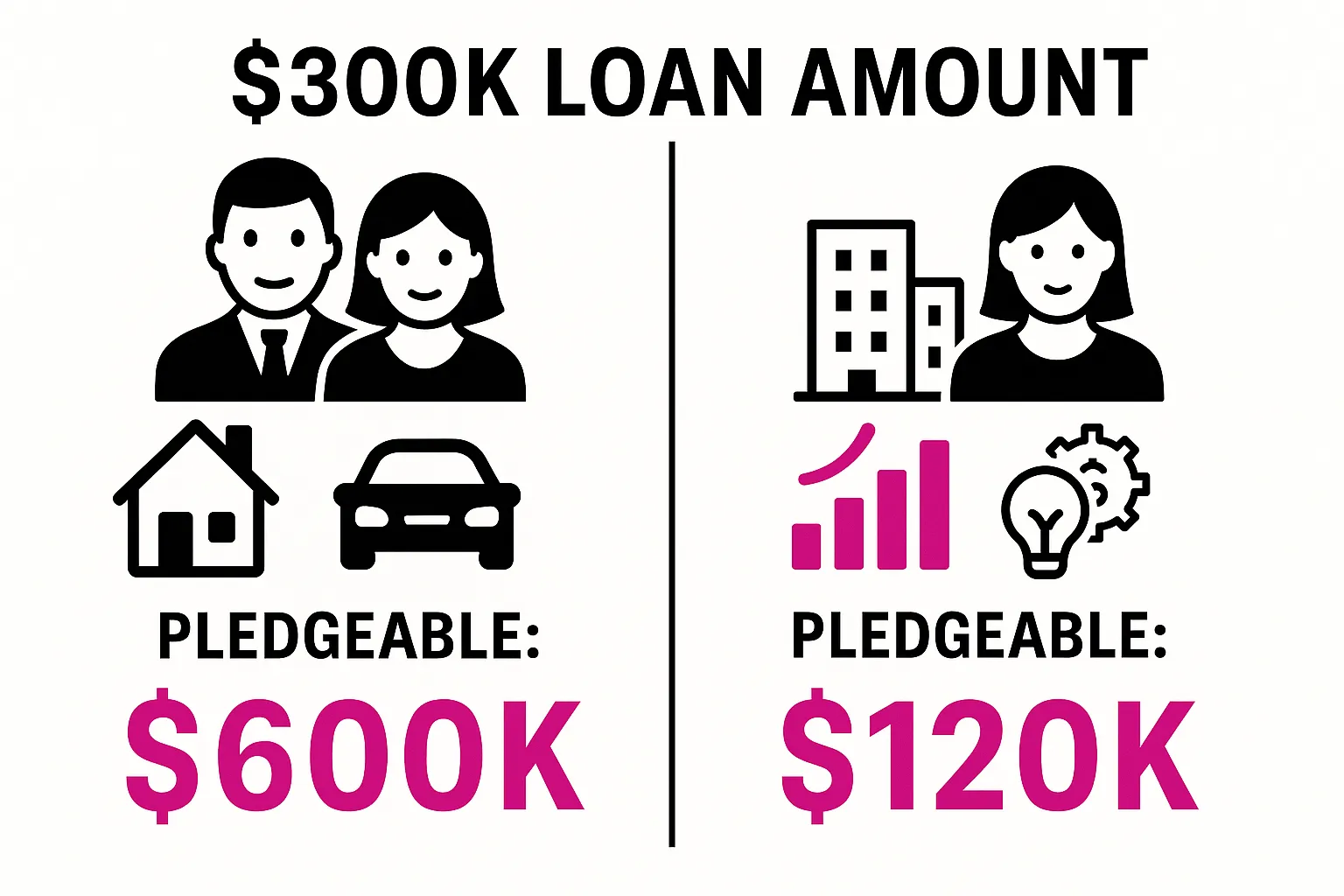

Founder A (married, dual-income household):

- Home equity: $250K

- Spouse’s brokerage account: $150K

- Investment property: $200K

- Total pledgeable: $600K → Covers a $500K loan comfortably

Founder B (single, sole-breadwinner):

- Rental apartment: $0 equity

- Retirement account: $120K (penalties if used before 59½)

- Business itself: the asset being funded

- Total pledgeable: $120K → Covers… 24% of a $500K loan

And the SBA won’t adjust the requirement. The lender won’t waive it. The only variable that changes is how much you get approved for — or whether you get approved at all.

Who Gets Hurt: The Profile of the Guarantor-Gapped Founder

This isn’t a niche problem. According to Census Bureau data, median net worth for single women is significantly lower than for single men or married households. The guarantor asymmetry hits hardest for:

- Divorced women who lost home equity in settlement. Courts split assets, but rarely consider future borrowing capacity when dividing property.

- Never-married founders who rent. In markets where homeownership requires $100K+ down, many successful business owners simply don’t own real estate.

- Primary breadwinners whose savings ARE the business runway. If your emergency fund is your operating capital, you can’t pledge it as collateral.

- Second-act founders who left corporate careers with a 401(k) but no liquid, pledgeable assets outside retirement accounts.

- Founders in asset-light industries (consulting, services, tech) where the business itself has minimal tangible collateral value.

The SBA lending system was designed in an era when business owners typically owned real estate. That era is over for many women founders.

What Lenders Actually See (And What They Won’t Tell You)

When your application hits underwriting, lenders evaluate several guarantee-related factors:

Guarantee coverage ratio: Your pledged personal assets divided by the loan amount. Below 0.5:1, most lenders get uncomfortable. Below 0.3:1, expect a counter-offer or denial.

Unlimited vs. limited guarantee: Most SBA loans require unlimited personal guarantees — meaning you’re liable for the full loan amount regardless of what you pledged. Some lenders will negotiate a limited guarantee (capped at a specific dollar amount) for strong borrowers.

Collateral position: Lenders prefer first-lien position on pledged assets. If your home already has a mortgage, the available equity for a second-position lien is often minimal.

The quiet partial approval: When a lender offers you $200K instead of the $350K you requested, the explanation is often “your collateral supports this amount.” They don’t always say it plainly. They might say “based on our analysis” or “given current conditions.” But the math is collateral math.

This is why negotiating better loan terms starts with understanding what’s actually driving the terms you’re offered.

The Alternatives Most Founders Don’t Know Exist

The guarantee requirement isn’t going away. But there are structures that reduce its bite:

SBA Express Loans

- Up to $500K

- SBA guarantees 50% (vs 75-85% for standard 7(a))

- Because SBA covers less risk, some lenders are more flexible on collateral from the borrower

- Faster approval (36 hours vs weeks)

- Trade-off: slightly higher rates

Equipment-as-Collateral Carve-Outs

- When the loan is specifically for equipment, the equipment itself serves as collateral

- Works for: vehicles, machinery, technology, manufacturing equipment

- The asset secures itself — no additional personal pledge required for that portion

- Available through SBA 504 and conventional equipment financing

Guarantee Burn-Down Clauses

- Negotiable on some loans: your personal guarantee reduces as the loan balance decreases

- Example: guarantee drops from unlimited to $200K cap after 36 months of on-time payments

- Not standard — you have to ask. Most borrowers never ask.

- More common at community banks and CDFIs than at large institutions

Revenue-Based Lending

- No personal guarantee whatsoever

- Repayment as a percentage of monthly revenue (typically 2-8%)

- Higher cost (6-12% flat fee on borrowed amount)

- Requirements: usually $10K+ monthly recurring revenue, 6+ months in business

- Providers: Lighter Capital, Clearco, Pipe, Capchase

SBA Microloans

- Up to $50K through nonprofit intermediaries

- More flexible collateral requirements than standard SBA programs

- Often available through CDFIs with mission-driven underwriting

- Good for: first-time borrowers building a track record

The “Credit Stacking” Approach

Instead of one large guaranteed loan, some founders build capital access through multiple smaller vehicles that each have different (or no) guarantee requirements:

- $50K microloan (flexible collateral)

- $30K business line of credit (secured by receivables)

- $25K equipment lease (asset-secured)

- Combined: $105K in capital without a traditional personal guarantee structure

This isn’t a credit card trap — it’s intentional architecture of capital access across multiple secured and unsecured vehicles.

The Strategic Response: Building Collateral You Can Pledge

If you’re 12–18 months away from needing a guaranteed loan, you can build toward it:

The earmarked investment account. Open a brokerage account specifically designated as future loan collateral. Even $25K in a diversified index fund is pledgeable. Lenders can place a lien on investment accounts without you liquidating them.

Cash value life insurance. Whole life policies build cash value that can serve as collateral. Takes 3–5 years to become meaningful. Not right for everyone, but worth understanding.

Build business credit independently. The stronger your business credit profile, the less weight lenders place on personal collateral. A business with established trade lines, a strong Dun & Bradstreet score, and consistent revenue can sometimes qualify for reduced personal guarantee requirements.

Negotiate the structure, not just the amount. When a lender says “we need a personal guarantee,” ask:

- “Can we cap it at [specific dollar amount]?”

- “Can we include a burn-down clause after 24 months of performance?”

- “Would additional business collateral (equipment, AR) offset the personal guarantee?”

Know when to walk away. If the guarantee required exceeds 150% of the loan value — meaning you’re pledging $750K in personal assets for a $500K loan — the structure is exploitative, not standard. Get a second opinion from a different lender type.

The Bigger Picture

The personal guarantee requirement was designed for a world where business owners and property owners were the same people. Increasingly, they’re not — especially for women starting businesses later in life, after divorce, or in asset-light industries.

The National Women’s Business Council has documented this structural gap. The Federal Reserve’s research confirms that collateral requirements are a primary driver of gender gaps in loan outcomes. The data is clear.

What’s not clear is whether policy will catch up. In the meantime, the strategies above aren’t workarounds — they’re the actual playbook for navigating a lending system that wasn’t designed with your household structure in mind.

The guarantee asymmetry is real. But it’s not a dead end — it’s a design constraint you can work around, once you see it clearly.