Your largest client just defaulted on a $40K invoice. Your walk-in freezer died and replacement costs $28K. Tariffs spiked your material costs 15% overnight and you have purchase orders to fulfill. You need cash — not next month, not after a 6-week application process. This week.

This is when women business owners make the most expensive financial decisions of their lives. Not because the options don’t exist, but because they don’t know which option fits their situation — and the wrong choice at the wrong moment can cost more than the crisis itself.

This is your triage guide. Print it. Bookmark it. Reference it when you’re calm so you’re prepared when you’re not.

The Decision Framework: Three Axes

Every emergency capital option exists somewhere on three scales:

- Speed: How fast can cash hit your account? (24 hours → 30+ days)

- Cost: What’s the effective annual cost? (0% → 150%+ APR)

- Long-term damage: What does this do to your business in 12 months? (Nothing → catastrophic)

The mistake most founders make: optimizing for speed alone. The fastest option is almost always the most expensive. Your job is to find the fastest option that your situation actually requires — which might be slower than you think.

Ask yourself: Do I need cash in 24 hours? Or do I need certainty that cash is coming in 7 days? Those are different problems with different solutions.

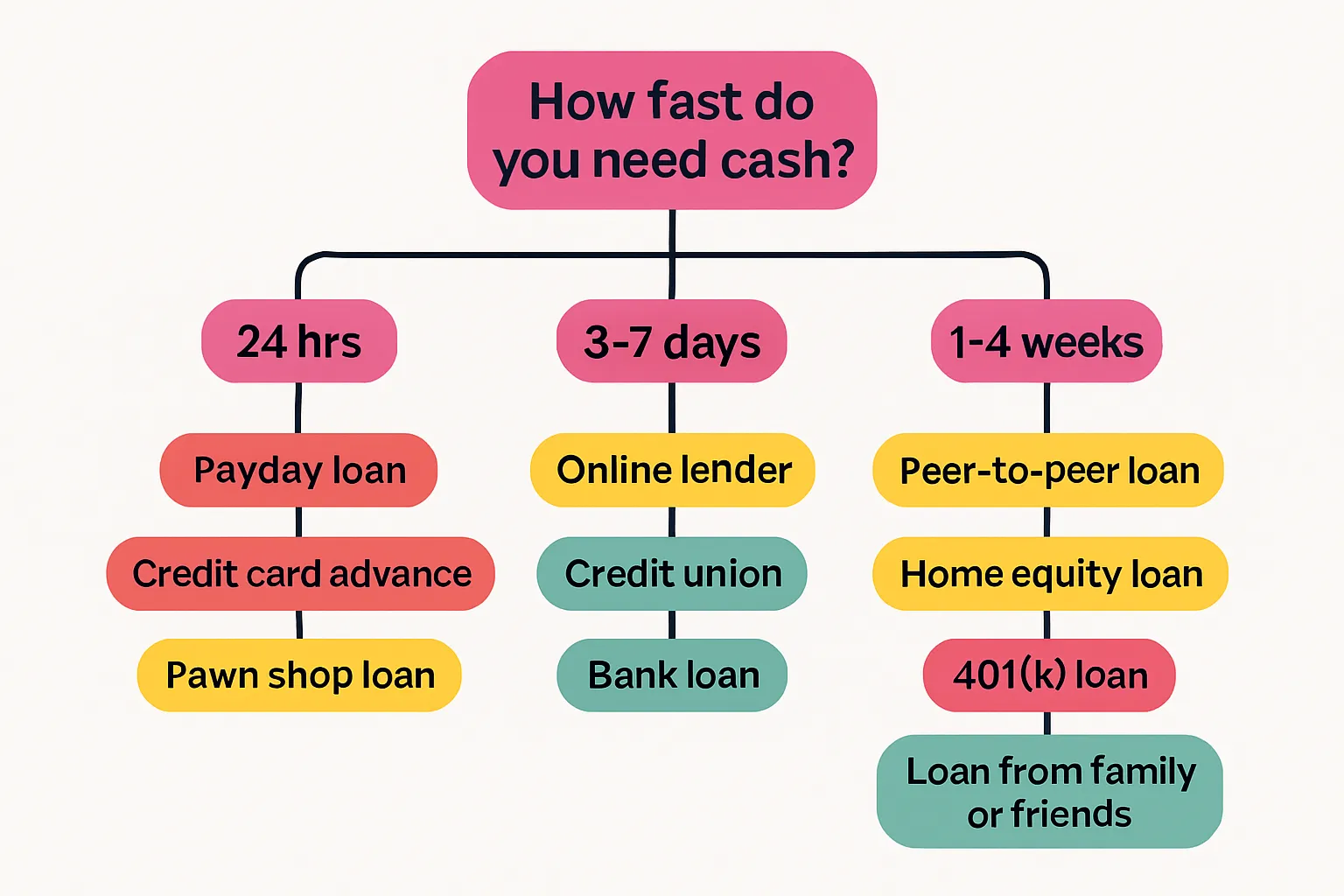

Tier 1: Cash in 24-48 Hours

Business Line of Credit (if already established)

- Speed: Instant (draw online, same-day)

- Cost: Prime + 1-3% (currently ~10-12% APR)

- Damage: None — this is what it’s for

- Requirement: Must already exist. You cannot open one during a crisis.

- The lesson: Open a line of credit when you don’t need it. Approval is easier when you’re not desperate.

Invoice Factoring (if you have outstanding B2B receivables)

- Speed: 24-48 hours for first funding (after onboarding, which takes 3-5 days initially)

- Cost: 1-5% per invoice (not annualized — flat fee per transaction)

- Damage: Low to moderate — you lose margin on those invoices, but preserve cash flow

- Requirement: Outstanding invoices from creditworthy business customers

- Best for: B2B service companies with $20K+ in outstanding receivables

- Providers: BlueVine, Fundbox, altLINE, Triumph Business Capital

Revenue-Based Advance

- Speed: 48-72 hours

- Cost: 6-12% flat fee on total amount (not annualized — you pay back principal + fee)

- Damage: Low — repayment flexes with revenue; if revenue drops, payments shrink

- Requirement: Usually $10K+ monthly recurring revenue, 6+ months operating history

- Providers: Clearco, Pipe, Capchase, Lighter Capital

- Best for: SaaS, subscription, or recurring-revenue businesses

Merchant Cash Advance (THE NUCLEAR OPTION)

- Speed: 24-48 hours, minimal documentation

- Cost: 40-150% effective APR. Read that again: forty to one hundred fifty percent.

- Damage: SEVERE. Daily automatic debits from your bank account. Stacking multiple MCAs is how businesses die.

- When it’s justified: Almost never. Only if the alternative is literally closing tomorrow AND you have a confirmed revenue event within 30 days that will cover repayment.

- The rule: If you’re considering an MCA, exhaust every other option on this list first. The MCA trap has destroyed more women-owned businesses than the crises that drove them to it.

Tier 2: Cash in 3-7 Days

Online Lenders (OnDeck, Kabbage/American Express Business Line, Fundbox)

- Speed: 3-5 business days from application to funding

- Cost: 15-45% APR depending on credit profile and term

- Damage: Moderate — expensive but predictable. Fixed payments, no surprises.

- Requirement: 1+ year in business, $100K+ annual revenue, 600+ credit score

- Best for: Established businesses that don’t qualify for (or can’t wait for) bank loans

- Note: Women-owned businesses see 61% approval at online lenders — the narrowest gender gap in lending

Equipment Financing

- Speed: 3-7 days (faster than general business loans because the asset secures itself)

- Cost: 5-15% APR

- Damage: Low — the equipment is the collateral, no personal guarantee on the equipment portion

- Requirement: The need must be specifically for equipment

- Best for: Equipment failure emergencies, vehicle replacement, technology upgrades

Purchase Order Financing

- Speed: 5-7 days

- Cost: 1-6% per month of the PO value (expensive, but short-duration)

- Damage: Low-moderate — you’re borrowing against confirmed future revenue

- Requirement: A confirmed, written purchase order from a creditworthy customer

- Best for: Product businesses that won a big order but can’t fund production

CDFI Emergency Programs

- Speed: 5-10 days (some have expedited emergency tracks)

- Cost: Below-market rates (often 5-8% APR)

- Damage: Minimal — mission-driven lenders with flexible terms

- Requirement: Must be in CDFI’s service area, meet mission criteria (most women-owned businesses qualify)

- Limitation: Funding amounts may be smaller ($10K-$100K typically)

Tier 3: Cash in 1-4 Weeks (Start Now, Not During Crisis)

SBA Express Loan

- Speed: Approval in 36 hours, but funding in 2-3 weeks

- Cost: Prime + 4.5-6.5% (currently ~13-15% APR)

- Damage: Minimal — standard SBA terms, reasonable rates

- Amount: Up to $500K

- Requirement: Existing banking relationship, standard SBA eligibility

- Best for: Predictable crises (you can see it coming 2-3 weeks out)

Community Bank Term Loan

- Speed: 2-4 weeks from application to funding

- Cost: 6-10% APR (best rates available for small business)

- Damage: None — this is healthy debt

- Requirement: Existing banking relationship, 2+ years in business, strong financials

- Best for: Businesses with established bank relationships who can plan slightly ahead

Vendor Payment Negotiation (Not Cash — But Buys Time)

- Speed: Immediate (one phone call)

- Cost: Free (usually)

- Damage: None if communicated professionally

- The script: “We’re experiencing a temporary cash flow timing issue. Can we extend payment terms to net-60 [or net-90] on this invoice?” Most vendors prefer late payment to losing a customer.

- Best for: Buying 30-60 days of breathing room while you secure actual financing

The “Never Do This” List

Some emergency capital decisions create problems worse than the crisis:

- Stacking multiple MCAs. The second MCA sees the first one’s daily debit and charges accordingly. Compound effective APR can exceed 300%. This is how businesses enter death spirals.

- Payday or personal loans for business use. Predatory rates + doesn’t build business credit + personal liability exposure.

- Raiding retirement accounts. 10% early withdrawal penalty + income tax + permanent loss of compound growth. A $50K 401(k) withdrawal costs you ~$150K in future retirement value.

- Missing payroll to cover vendor payments. Legal exposure in most states + employees leave + reputation damage that outlasts any cash crisis.

- Maxing personal credit cards for business expenses. Destroys personal credit score, triggers high-interest revolving debt, and doesn’t build business credit.

The one exception: Sometimes closing the business IS the right financial decision. If the crisis requires more capital than the business can ever repay, the least-damaging option might be an orderly wind-down rather than expensive rescue debt. That’s not failure — it’s financial intelligence.

Build the Tree Before the Crisis

The time to research emergency capital is when you don’t need it:

This week:

- Open a business line of credit (approval takes 2-4 weeks, but once open, it’s instant access)

- Identify 2-3 invoice factoring companies and get pre-qualified

- Find your nearest CDFI and understand their programs

This month:

- Research revenue-based advance providers if you have recurring revenue

- Ask your bank about their expedited lending programs

- Know your vendor payment terms and which ones have flexibility

This quarter:

- Build toward 90 days of operating reserves so you need emergency capital less

- Establish relationships with at least two lender types (bank + alternative)

- Review this decision tree and know your top 2 options cold

The founders who survive cash crises aren’t the ones who find the best emergency loan. They’re the ones who built the infrastructure — credit lines, relationships, reserves, knowledge — before the emergency arrived.

The Decision in Practice

When crisis hits, answer these four questions:

- How much do I need? (Be precise — don’t borrow more than necessary)

- How fast do I actually need it? (Not “ASAP” — what’s the real deadline?)

- What’s my repayment capacity? (What monthly payment can I sustain for 12-24 months?)

- What’s my confirmed future revenue? (Do I have contracts, POs, or receivables that guarantee repayment?)

Match your answers to the tier above. If your real deadline is 10 days (not 24 hours), you’ve just unlocked Tier 2 options that cost 1/10th what Tier 1 emergency options cost.

The most expensive word in emergency financing is “immediate” — and often, you don’t actually need immediate. You need certain. Those are different price points.

Crisis is not the time to learn your options. That’s now.