Your bank isn’t rejecting you because you’re not ready. It’s rejecting you because it was never built to say yes.

You’ve had your business checking account at the same bank for three years. You applied for a $150K line of credit. You were denied — or worse, ghosted. The relationship manager you met once can’t remember your company name. And you’re still depositing revenue there every month like nothing happened.

Here’s the number that should make you furious: community banks approve small business loans at 53%. Large national banks? 13–14%. That’s not a gap — that’s a completely different business model. If you’re banking at a big-four institution and wondering why you can’t get funded, the problem might not be your application. It might be your address book.

The Red Flags You’re Ignoring

Your current banking relationship is costing you if:

- Your loan application has been “in review” for 3+ months. At community banks and CDFIs, a decision takes 2–6 weeks. If your application is sitting in a queue, you’re not being evaluated — you’re being deprioritized.

- You were denied with no explanation beyond “insufficient history.” This often means “we don’t have a lending relationship with you” — which is different from “you don’t qualify.”

- Your relationship manager doesn’t know your business name. At large banks, you’re a file number. At community banks, you’re a business they see in their own community.

- You’ve never been offered a business credit product proactively. Banks that want to lend to you will suggest products before you ask. Silence isn’t neutral — it’s a signal.

- Your deposits exceed $10K/month and you’ve never been invited to a portfolio review. You’re providing free capital to an institution that won’t return the favor.

If three or more of these are true, you don’t have a banking relationship. You have a checking account.

The Approval Rate Reality: Where Women Actually Get Funded

The Federal Reserve’s Small Business Credit Survey consistently shows that lender type matters more than almost any borrower characteristic:

- Community banks: 53% approval rate, per FDIC data. Relationship-driven underwriting. They know the local market and make judgment calls.

- Credit unions: Member-owned, often more flexible on collateral requirements. Business lending programs vary — some are excellent, some barely exist. Check the NCUA credit union directory first.

- CDFIs (Community Development Financial Institutions): Mission-driven lenders designed specifically for underserved borrowers, including women-owned businesses. Below-market rates, flexible terms, hands-on support.

- Online lenders: 61% approval for women-owned businesses (vs 67% for men) — the narrowest gap in lending. Faster, but more expensive.

The “dual banking” strategy works for many founders: keep your day-to-day operations at whatever institution handles transactions well, but build your lending relationship at a community bank or CDFI that actually wants to fund you.

The Seasoning Problem: Why You Can’t Switch and Borrow Same-Day

Here’s what nobody tells you about changing banks: the new institution needs time with you before they’ll lend.

Most lenders want 3–6 months of deposit history before they consider you a “relationship client” for lending purposes. This is called seasoning, and it’s why the bank breakup needs to happen before you need capital.

What counts as a “relationship” varies by institution, but generally:

- Deposit volume: Consistent business revenue flowing through the account (not occasional transfers)

- Account age: Minimum 90 days, preferably 180

- Product cross-sell: Having multiple products (checking + savings + merchant services) signals commitment

- Face time: Having met a business banker in person at least once

The strategic move: open the new account 6 months before your planned loan application. If you think you’ll need capital in Q1 2027, start the new banking relationship in Q3 2026. The best time to switch was six months ago. The second best time is today.

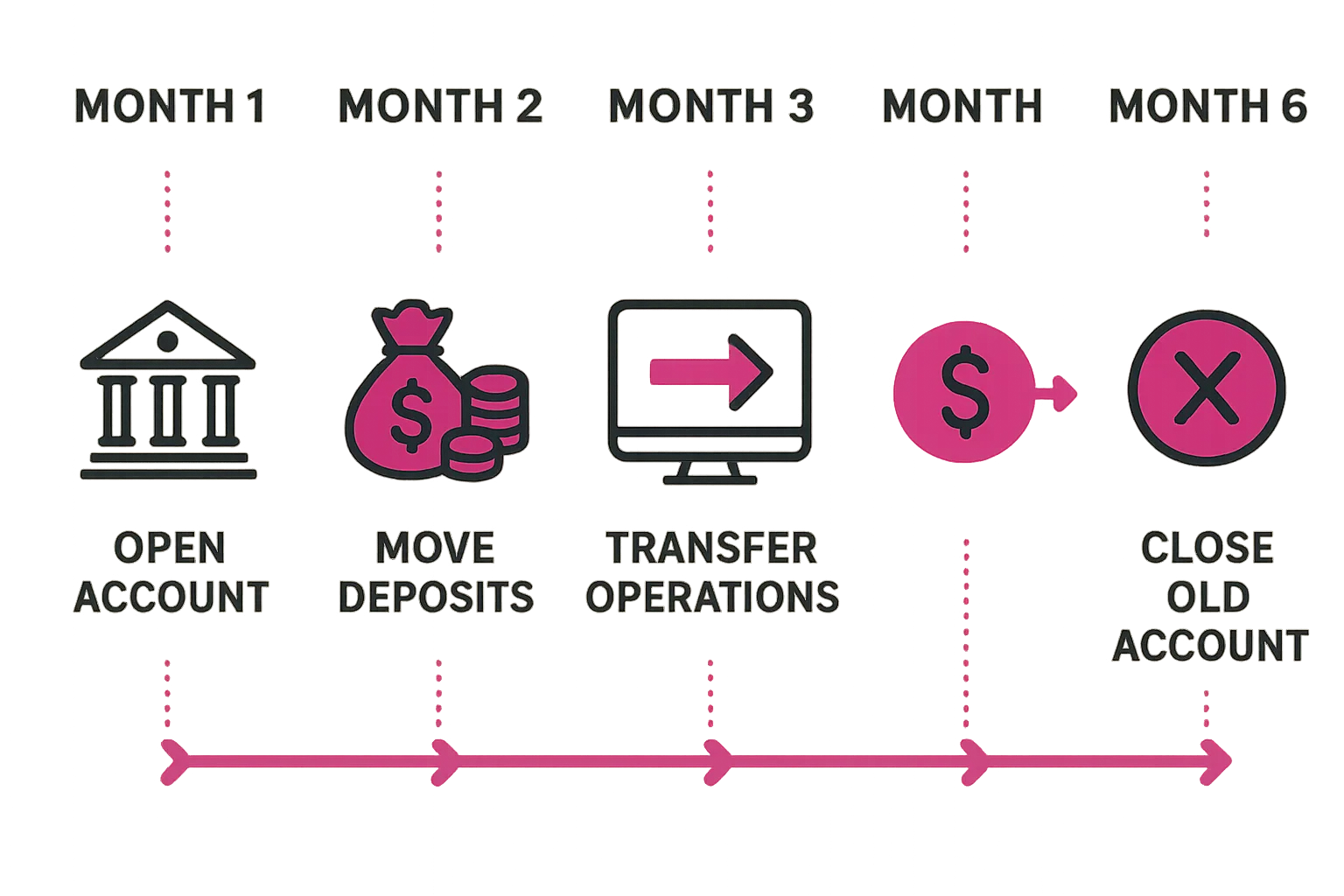

The Transition Playbook: What to Move First

Don’t rip the bandaid. Stage the transition over 60–90 days:

Stage 1 (Week 1–2): Open and seed

- Open business checking at new institution

- Route 30–50% of incoming revenue to new account

- Set up online banking and mobile deposit

Stage 2 (Week 3–6): Move operations

- Transfer payroll processing to new account

- Redirect vendor auto-payments

- Update billing info with your top 5 clients

Stage 3 (Week 6–10): Move the money

- Transfer credit card processing / merchant services

- Move business savings or money market account

- Update tax payment accounts (federal and state)

Stage 4 (Week 10–12): Clean close

- Confirm ALL auto-debits have cleared from old account

- Wait one full billing cycle to catch stragglers

- Close old account (get written confirmation)

Critical rule: Do NOT close or reduce existing credit lines at the old institution until new ones are established. An open credit line — even unused — builds your business credit profile. Closing it can actually hurt your score.

How to Position Yourself at the New Institution

The first 30 days at a new bank set the tone for the entire relationship. Do this right:

Week 1: Request a meeting with a business banker (not a teller, not customer service — a commercial or business banking specialist). Most community banks will schedule this gladly. Bring:

- 2 years of tax returns

- Current P&L and balance sheet

- Brief business summary (1 page)

- Your 12-month revenue projection

The meeting: Don’t ask for a loan. Ask this question instead:

“What does your institution need to see from me over the next 6 months to consider me for a $[amount] [product type]?”

This does three things: it signals you’re planning ahead (not desperate), it tells you exactly what to build toward, and it creates accountability — they’ve now told you the goalposts.

Week 2–4: Follow up with whatever they requested. If they said “we’d like to see 3 months of deposits,” start routing revenue immediately. If they mentioned specific documentation, provide it early.

Resources like Lendesca can help you identify institutions with track records of funding women-owned businesses in your revenue range — useful when you’re choosing between multiple community banks in your area.

After a loan denial at your current bank, the instinct is to fix yourself. Sometimes the fix is fixing your address book.

The Timeline: Bank Breakup to First Loan

| Month | Action | Goal |

|---|---|---|

| 1–2 | Open account, begin deposits, meet banker | Establish presence |

| 3–4 | Full transition of operations, consistent deposits | Build history |

| 5–6 | Formal loan conversation, reference relationship | Leverage seasoning |

The math: 6 months of intentional positioning vs. years of rejection at the wrong institution.

The women who get funded aren’t always better-qualified. Often, they’re just better-banked. They found institutions that evaluate applications through a lens built for businesses like theirs, where a conversation with a banker replaces an algorithm, and where 53% doesn’t just mean better odds — it means someone actually looked at the file.

Once you have the right banking relationship, negotiating your loan terms becomes a real conversation instead of a take-it-or-leave-it offer.

Your bank should want to lend to you. If it doesn’t, leave.