Your business took years to build. The revenue, the relationships, the reputation — all of it accumulated through decisions you made, risks you took, and nights you worked when everyone else stopped. Then your marriage ends, and suddenly a court is deciding whether half of it belongs to someone else.

This happens to women founders more than anyone talks about. The legal and financial system treats a business like any other marital asset — something to divide, not something to protect. And most of what’s written about it is authored by divorce attorneys, for divorce attorneys, explaining how to litigate after the damage is already done.

This guide is written for the founder. It explains the financial mechanics of what actually happens to a business in divorce, what you can do before you ever need it, and what to do if you’re already in the middle of it. No sympathy. Just strategy.

Why This Piece Exists (And Why Nobody Else Wrote It)

Roughly 40-50% of marriages in the United States end in divorce. That statistic has been stable for decades. What’s changed is the number of women who enter those marriages as business owners — or who build businesses during them.

When a founder couple divorces, the business doesn’t get to stay out of it. Courts treat business interests as marital assets subject to division. The valuation, the ownership structure, the debt obligations — all of it goes into the pot. And because most women founders face the structural funding gap already stacked against them, they often have fewer liquid assets to use as offsets in a settlement. That means the business itself becomes the most negotiable item.

The existing content ecosystem fails founders completely. Search “business divorce” and you’ll find attorney-written articles explaining divorce law, not business strategy. Financial advisors who specialize in divorce call themselves “CDFAs” and mostly serve high-net-worth individuals negotiating investment portfolios. Nobody is sitting down with a woman who owns a $2M HVAC company or a $800K consulting practice and explaining exactly what’s at stake and what levers she has.

This guide fills that gap. It is not about expecting your marriage to fail. It is about understanding the financial structure that protects what you’ve built — the same way you insure a business vehicle before you get in an accident.

What’s at Stake — How Courts Value Your Business

Before you can protect anything, you need to understand what courts are actually looking at. The rules are not uniform. Where you live matters enormously.

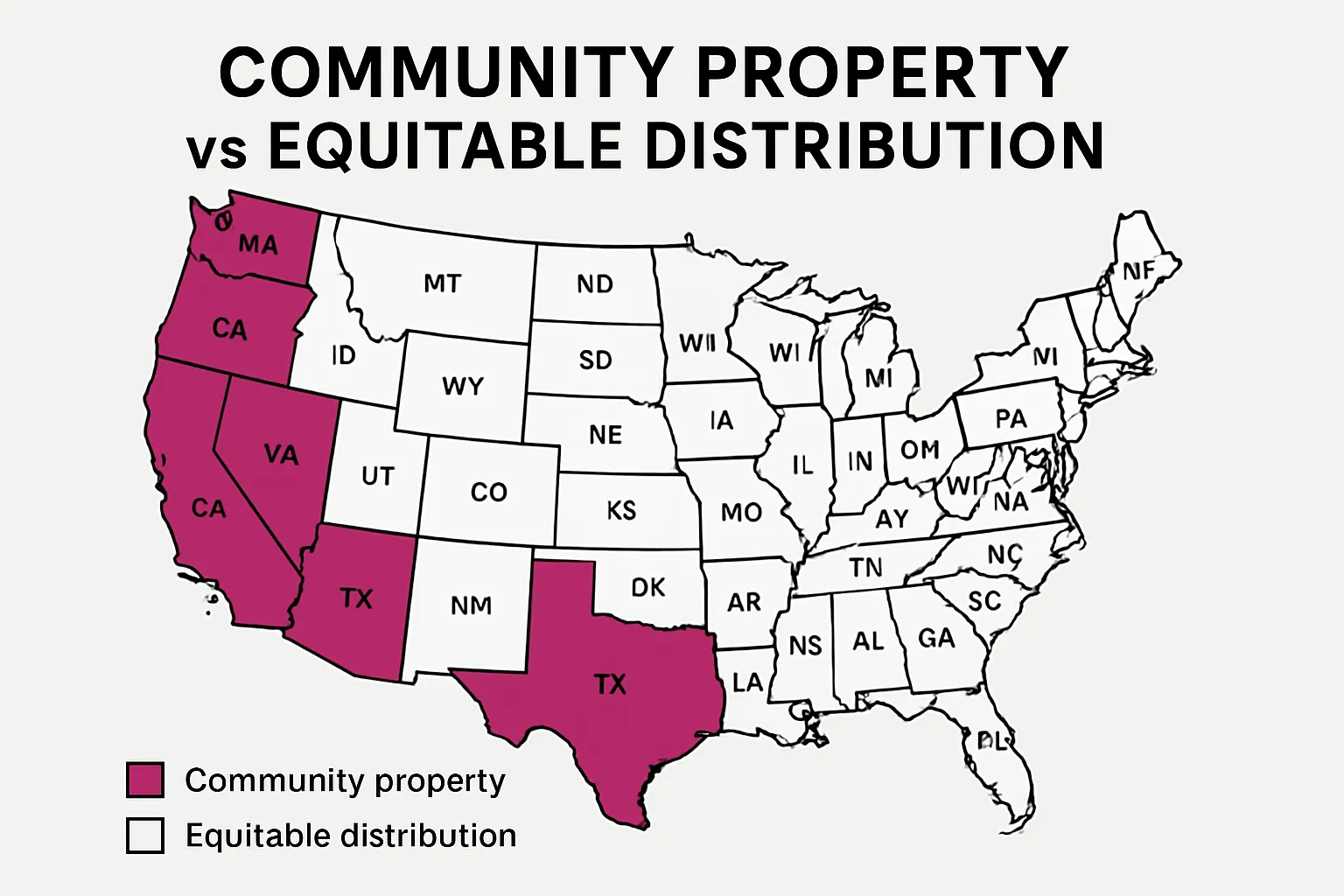

Community Property vs. Equitable Distribution

The United States uses two fundamentally different frameworks for dividing marital assets:

Community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, Wisconsin, plus Alaska by opt-in) treat most assets acquired during marriage as jointly owned 50/50. This includes business growth — if your business increased in value during the marriage, that appreciation is presumed to be community property regardless of who did the work.

Equitable distribution states (the remaining 41 states plus DC) divide assets “fairly” — which does not mean equally. Courts consider each spouse’s contributions, earning capacity, length of marriage, and other factors. Equitable can mean 60/40 or 70/30. It also means more room to argue.

If you’re in California and your business doubled during your marriage, plan on that doubling being on the table. If you’re in Massachusetts, there’s more room to argue — but less certainty.

How Courts Value a Business

Courts typically use three valuation methodologies, often in combination:

Asset-based valuation — Total business assets minus liabilities. Useful for asset-heavy businesses (real estate, manufacturing). Often undervalues service businesses where the value is in relationships, not equipment.

Income-based valuation — Capitalizes future earnings based on current profitability. Calculated using a capitalization rate applied to normalized earnings. This is where the “adjustments” happen — and where your expert witness and your spouse’s expert witness will disagree.

Market-based valuation — Compares your business to recent sales of similar businesses. Works well when comparable transactions exist. Thin for specialized industries.

Your spouse’s attorney will push for whichever methodology produces the highest number. You need your own valuation expert — someone certified by the National Association of Certified Valuators and Analysts (NACVA) — not just the court-appointed one.

Active vs. Passive Appreciation

This distinction is worth understanding precisely, because it’s where founders lose the most ground.

Passive appreciation is business value growth driven by market forces — inflation, industry trends, economic tailwinds — that would have happened regardless of your effort. Courts generally treat this as separate property, even in community property states.

Active appreciation is growth driven by your work during the marriage — your sales relationships, the operational improvements you made, the team you built. In most states, this active appreciation is considered marital property even if you started the business before the wedding.

Translation: You could own a business outright before you get married, grow it from $500K to $3M during the marriage, and a court can rule that the $2.5M in growth is subject to division.

The Goodwill Problem

Many service businesses — consulting firms, medical practices, agencies, financial advisory firms — have significant “goodwill” value: the business is worth more than its hard assets because of reputation and relationships.

Courts distinguish between personal goodwill (tied to you specifically — your skills, your reputation, your relationships) and enterprise goodwill (attached to the business entity itself, transferable to a new owner). Some states split enterprise goodwill as a marital asset. Personal goodwill is usually treated as separate property.

The line between them is genuinely contested. And your state’s case law on this point can make a six-figure difference in your settlement.

The Worst-Case Scenario

If negotiations fail and neither party can fund a buyout, courts can — and occasionally do — order a business sold and the proceeds split. This is rare, but it happens. Understanding that this outcome is legally possible is important context for every decision that follows.

Proactive Protection — Before You Need It

The most effective protection for your business in divorce is structure you put in place before divorce is on your mind. If you’re currently in a stable marriage and building a business, this section is written for you.

Prenuptial and Postnuptial Agreements

A well-drafted prenuptial agreement is the single most effective tool for protecting your business. It defines, in advance, which assets are separate property and what happens to business appreciation in the event of divorce.

If you’re already married without a prenup, a postnuptial agreement accomplishes the same thing. Courts scrutinize them more carefully — both spouses need independent counsel, there must be full financial disclosure, and there can’t be duress — but they’re enforceable in most states.

What makes these agreements unenforceable:

- Signed under pressure or immediately before the wedding

- One party didn’t have independent legal counsel

- No financial disclosure

- Terms that are unconscionably one-sided

The Uniform Premarital Agreement Act, adopted in 28 states, provides the framework for what’s required. Understanding your state’s version of this law tells you what you need in the document.

Entity Structure as Protection

Your business entity structure is a legal moat. Used correctly, it makes it harder for a court to simply hand half your business to a spouse.

Specific tools:

- LLC operating agreements with transfer restrictions — language that prohibits transfer of membership interests to non-members without unanimous consent of existing members

- Buy-sell agreements in S-corp bylaws that trigger a mandatory buyout if any owner attempts to transfer shares, including through divorce proceedings

- Right of first refusal clauses requiring the business to have the opportunity to purchase any transferred interest before it goes to a third party (including a divorcing spouse)

These don’t make your business invisible to a court — the economic value is still a marital asset. But they do make a court-ordered transfer of actual ownership substantially harder, which pushes toward a cash buyout rather than a forced ownership split.

The SBA’s guidance on business entity structures covers the baseline mechanics if you’re selecting or restructuring your entity.

Financial Separation: Stop Commingling

Courts look at how you’ve managed business finances as evidence of whether the business is truly separate. The more you’ve blurred the lines, the more a court will blur them back.

Non-negotiable practices:

- Separate business bank accounts — never personal funds in business accounts or vice versa

- Pay yourself a market-rate salary — and document it. Founders who underpay themselves to grow the business create a problem: courts then argue the marital lifestyle was subsidized by the business, which inflates what’s considered marital

- Never pay personal expenses from business accounts — not one Netflix subscription, not one grocery run

- Document capital contributions — if you put personal savings into the business, write a formal loan or document it as a capital contribution with dates and amounts

These habits do double duty: they make your books look professional to lenders, and they create a clear forensic trail if a court ever examines your financials.

Documentation: Build Your Paper Trail Now

If you started your business before marriage, document its pre-marital value. A business valuation at the time of marriage becomes the baseline “separate property” figure — the starting point courts use to calculate how much appreciation occurred during the marriage.

Keep:

- Tax returns from before and during marriage

- Business bank statements showing pre-marital balances

- Capitalization records showing your initial investment

- Records of any loans you took personally to fund the business

The harder it is for a spouse’s attorney to argue that the business value at marriage was zero, the better your position.

Key Person Insurance

Structure key person life insurance policies with the business entity as beneficiary, not your spouse. This is standard business risk management — and it matters in divorce because insurance proceeds designated to a spouse can complicate asset division and business continuity.

Review your existing policies. If your spouse is named as beneficiary on any business-related insurance, talk to an attorney about your options.

If You’re Already in It — The Divorce Financial Playbook

If you’re reading this mid-divorce, skip the retrospective. Here’s what to do in sequence.

Step 1: Get a Forensic Accountant First

Before you hire a divorce attorney, hire a forensic accountant who specializes in business valuations in divorce. You need to know what you’re working with before you start negotiating.

A forensic accountant will:

- Reconstruct your business’s financial history

- Identify what’s likely to be considered marital vs. separate property in your state

- Spot any issues in your financials that could be used against you

- Tell you the realistic range of business valuations your spouse’s expert might use

Walking into a divorce proceeding without understanding your business’s financial picture is like negotiating a contract you haven’t read.

Step 2: Get Your Own Independent Valuation

Never rely solely on the valuation commissioned by your spouse’s team. Hire your own certified business valuator — ideally someone credentialed through NACVA or the American Society of Appraisers — to produce an independent report.

The gap between two legitimate valuations of the same business can be enormous. Methodology choices, which earnings years to normalize, how to treat owner compensation, whether to apply discounts for lack of marketability — these are all judgment calls, and they add up to real dollars.

Your expert and their expert will likely disagree. The settlement or court decision will land somewhere between the two numbers. Starting with your own number means you control the floor.

Step 3: Know Your Options

There are four basic outcomes for a business in divorce:

Buyout — You pay your spouse for their share of the business’s marital value. The business stays yours. This is usually the best outcome for a founder who wants to keep operating.

Offset — You give up other marital assets (real estate equity, retirement accounts, cash) equal to the business’s value. The business stays yours without a cash payment. Requires having other significant assets.

Structured settlement — You pay out the buyout over time through installment payments. Preserves cash flow but creates an ongoing financial obligation to an ex-spouse.

Continued co-ownership — Rare. Almost always bad. Do not enter a business partnership with someone you’re divorcing unless there is absolutely no other option.

Step 4: Protect Cash Flow During Proceedings

Divorce proceedings take time — often 12 to 24 months for contested cases involving a business. During that period, your business needs to keep operating. Do not let the legal process bleed your working capital.

Practical steps:

- Maintain cash reserves separately from any business account your spouse has visibility into (with legal guidance to ensure this is permissible in your jurisdiction)

- Don’t make major capital expenditures during proceedings without legal counsel

- Keep payroll and vendor relationships stable — operational disruption hurts your valuation and your leverage

- Document every business decision during proceedings in writing

Step 5: Refinance Business Debt to Remove Your Spouse

If your spouse is a co-signer or personal guarantor on any business debt, that obligation follows them legally until it’s removed. Refinancing those loans in your name alone — or removing the guarantee entirely — is a clean break that also clarifies your business’s true debt picture.

Lendesca is one resource for business refinancing that can help owners restructure existing debt during or after a divorce, separating personal from business obligations cleanly. Talk to your attorney before initiating any refinancing to ensure timing and structure align with your settlement strategy.

Separately, review IRS Publication 504 for the tax implications of transfers between divorcing spouses — including business transfers, which have specific treatment under tax law that affects how you structure any buyout or debt refinancing.

What Not to Do

Courts have seen every financial trick. Do not:

- Hide assets or underreport revenue in anticipation of divorce

- Suddenly pay yourself a much higher or lower salary to manipulate the business valuation

- Transfer ownership to family members to reduce your apparent interest

- Create fictitious expenses to suppress profitability

These tactics backfire badly. Courts penalize them during settlement and impose sanctions in litigation. The forensic accountant your spouse hires will find the anomalies — their job is specifically to look for them.

The Buyout — How to Keep Your Business and Make It Fair

The buyout is typically the best outcome for a founder who wants to preserve the business. Here’s how it actually works.

Buyout Structures

Lump sum — You pay the agreed value upfront. Clean break, no ongoing obligations, but requires significant liquidity. Best if you have cash reserves or can access a business loan.

Installment payments — You pay out the buyout over time, typically 3-5 years. Preserves your immediate cash position but creates a long-term obligation. If the business struggles, you still owe the payments.

Asset offset — You surrender other marital assets (home equity, retirement accounts, investment portfolio) in exchange for keeping the business at full value. Requires having offsetting assets of comparable value.

Funding the Buyout

Sources founders actually use:

- Business cash reserves (if the business can support it without strangling operations)

- A business acquisition or growth loan taken against the business’s assets

- A personal loan using non-business assets as collateral

- Retirement account offsets (note: there are specific rules about QDRO — qualified domestic relations orders — that govern how retirement accounts can be used in divorce settlements)

Tax Implications

The buyout structure has real tax consequences. A lump sum payment from business funds may trigger tax differently than a transfer of business equity. Installment payments have interest implications. Asset offsets involving real estate or retirement accounts each have their own tax treatment.

Get a CPA — not just your accountant — involved before you finalize any buyout structure. The IRS Publication 504 covers the basics, but a CPA who handles divorce-related tax issues will know the nuances.

Where the Real Money Is Won

The most important negotiation in a business buyout is not the payment structure. It’s the valuation methodology.

A business valued on a 3x earnings multiple is worth half what it’s worth on a 6x multiple. Whether to use the last three years’ earnings or a normalized single year, whether to add back owner compensation or keep it as an expense, whether to apply a minority discount — these methodological choices drive the final number more than almost anything else.

This is where negotiating loan terms experience translates directly: understanding what the other side wants from the numbers and finding the methodological choices that produce a fair outcome for you, not just for them.

You need an attorney who understands business valuation, not just family law. The American Academy of Matrimonial Lawyers maintains a directory of attorneys who specialize in high-asset divorce including business interests.

The Installment Trap

If you accept installment payments as the buyout structure, model the cash flow carefully. An installment obligation of $15,000/month to an ex-spouse is a fixed cost that doesn’t scale down if revenue drops. Make sure your business’s baseline cash generation — not its projected future growth — can support the payments through a realistic downturn scenario.

Get termination provisions drafted carefully. If the business experiences a genuine financial hardship (documented through financials), what happens to the payment schedule? Negotiate this before you sign, not after.

After the Divorce — Rebuilding Your Financial Foundation

The settlement is signed. The business is yours. Now the operational cleanup begins.

Update Every Legal Document

In the 30 days after your divorce is finalized:

- Update your LLC operating agreement or corporate bylaws to remove your ex-spouse from any listed roles

- Change all beneficiary designations — business insurance policies, retirement accounts, key person coverage

- Update your business’s power of attorney

- If your ex-spouse held any formal role in the business (officer, director, authorized signatory), file the appropriate paperwork to remove them

- Update bank account signatories immediately

Rebuild Business Credit Independently

If your business credit was built on or tied to your spouse’s personal credit history, that’s a liability in your new chapter. Start rebuilding business credit immediately and independently — establish trade lines, use a business credit card in the business’s name, and make sure your Dun & Bradstreet and Experian Business profiles are active and clean.

This matters because your ability to refinance, access capital, or negotiate vendor terms going forward depends on a credit profile that’s yours, not a co-borrower’s.

Re-establish Banking Relationships

If your primary banking relationship included your spouse as a signer, open a new primary business account at a different institution. This is not about hiding assets — it’s about establishing clean, independent banking relationships that reflect your business’s new ownership structure.

Brief your banker on the situation. A good commercial banker will help you rebuild your credit profile and flag the right products for your current situation.

The Emotional Dimension

Here’s the one place where the emotional reality matters strategically: business decisions made in the heat of divorce proceedings are often bad business decisions.

The desire to punish, to win every point, to never give an inch — these are human responses to a painful situation, but they prolong litigation, increase legal fees, and sometimes result in worse outcomes than a faster settlement would have produced.

The most financially effective divorce strategy is often the fastest one — reach a fair settlement, get back to running your business, and stop paying attorneys to negotiate while your competitors gain ground. This is cold-blooded logic, not acceptance of an unfair outcome. Know what you need to protect, negotiate hard for those things, and release what doesn’t matter.

The Next Chapter

Your business survived. Most don’t, not intact. The fact that you’re on the other side of this with your ownership structure clean is a win that deserves exactly five minutes of acknowledgment before you get back to work.

The Funding Playbook at HerCapital covers what comes next: rebuilding access to capital, growing through the next phase, and doing it without a structural disadvantage you didn’t create.

The funding gap is real and documented. The bias in the lending system is real and documented. None of that changed because you went through a divorce. What changed is that you now have a cleaner financial structure and a documented history of building something worth fighting for.

Use both.

Quick Reference: Divorce Protection Checklist

Before you need it:

- Prenuptial or postnuptial agreement drafted with independent legal counsel

- Business valuation at time of marriage documented and stored

- Transfer restrictions in operating agreement or bylaws

- Completely separate business and personal finances

- Market-rate salary documented

- Key person insurance naming business as beneficiary

If you’re in proceedings:

- Forensic accountant retained before anything else

- Independent business valuation commissioned

- Own legal counsel specializing in high-asset divorce retained

- Cash flow protected and documented

- Major expenditures paused pending legal guidance

- Business debt refinancing evaluated with counsel

After settlement:

- All legal documents updated

- All beneficiary designations changed

- Business credit being rebuilt independently

- New banking relationships established

- CPA reviewed tax implications of settlement structure

HerCapital does not provide legal or financial advice. This article is for informational purposes. Consult a qualified divorce attorney and financial advisor for guidance specific to your situation and jurisdiction.