Your runway is the number of months you can keep the business alive with zero incoming revenue. Not reduced revenue. Zero.

It’s the most important metric you probably don’t track. And it’s almost certainly shorter than you think.

According to JPMorgan Chase Institute research, the median small business holds only 14 days of cash buffer. For women-owned businesses — which access credit lines at lower rates and self-fund more frequently — the number skews even shorter.

Here’s why this matters beyond survival: lenders check your cash reserves before approving loans. Investors look for 12–18 months of runway. The SBA wants to see 3 months post-close minimum. Your runway isn’t just how long you can survive — it’s how much capital the system is willing to give you.

Short runway → emergency capital → expensive debt → shorter runway. It’s a trap. Here’s how to break it.

Your Runway Number: Calculate Your True Burn Rate

Runway isn’t “how much money is in my checking account.” It’s cash reserves divided by monthly burn at minimum viable operations.

Step 1: Calculate your fixed monthly costs

- Rent/lease payments

- Payroll (including yours) + payroll taxes

- Insurance premiums (health, liability, property)

- Loan/debt payments

- Software subscriptions

- Utilities and internet

Step 2: Add your variable minimums

- What are your variable costs at MINIMUM operations? (Not current spending — survival spending)

- Materials/COGS at reduced output

- Marketing at maintenance level

- Contract labor you can’t cut

Step 3: Don’t forget the hidden burns

- Quarterly estimated tax payments (divide annual by 12)

- Annual renewals that hit in specific months (licenses, certifications, insurance renewals)

- Seasonal revenue dips (calculate your worst month, not average)

Step 4: Your REAL number

- Total monthly burn = fixed + variable minimum + (hidden burns ÷ 12)

- Available cash reserves = business savings + accessible reserves (NOT operating checking, NOT retirement)

- Your runway = available cash reserves ÷ total monthly burn

Most founders who do this math for the first time discover their runway is 15–30 days. That’s not a business with reserves — that’s a business one bad month from crisis.

The gap between knowing your numbers and using them strategically starts right here.

The Benchmarks: What Lenders and Investors Expect

Your runway number communicates something specific to capital providers:

| Runway | What It Signals | What It Gets You |

|---|---|---|

| < 30 days | Operating at the edge, cash crisis likely | Denial or expensive emergency capital |

| 30–60 days | Surviving but not stable | Approval possible, but at higher rates |

| 60–90 days | Financially disciplined | Standard loan approval, reasonable terms |

| 90–180 days | Strategic reserve, optionality | Better rates, larger amounts, negotiating power |

| 180+ days | Investor-grade discipline | Best terms available, proactive offers from lenders |

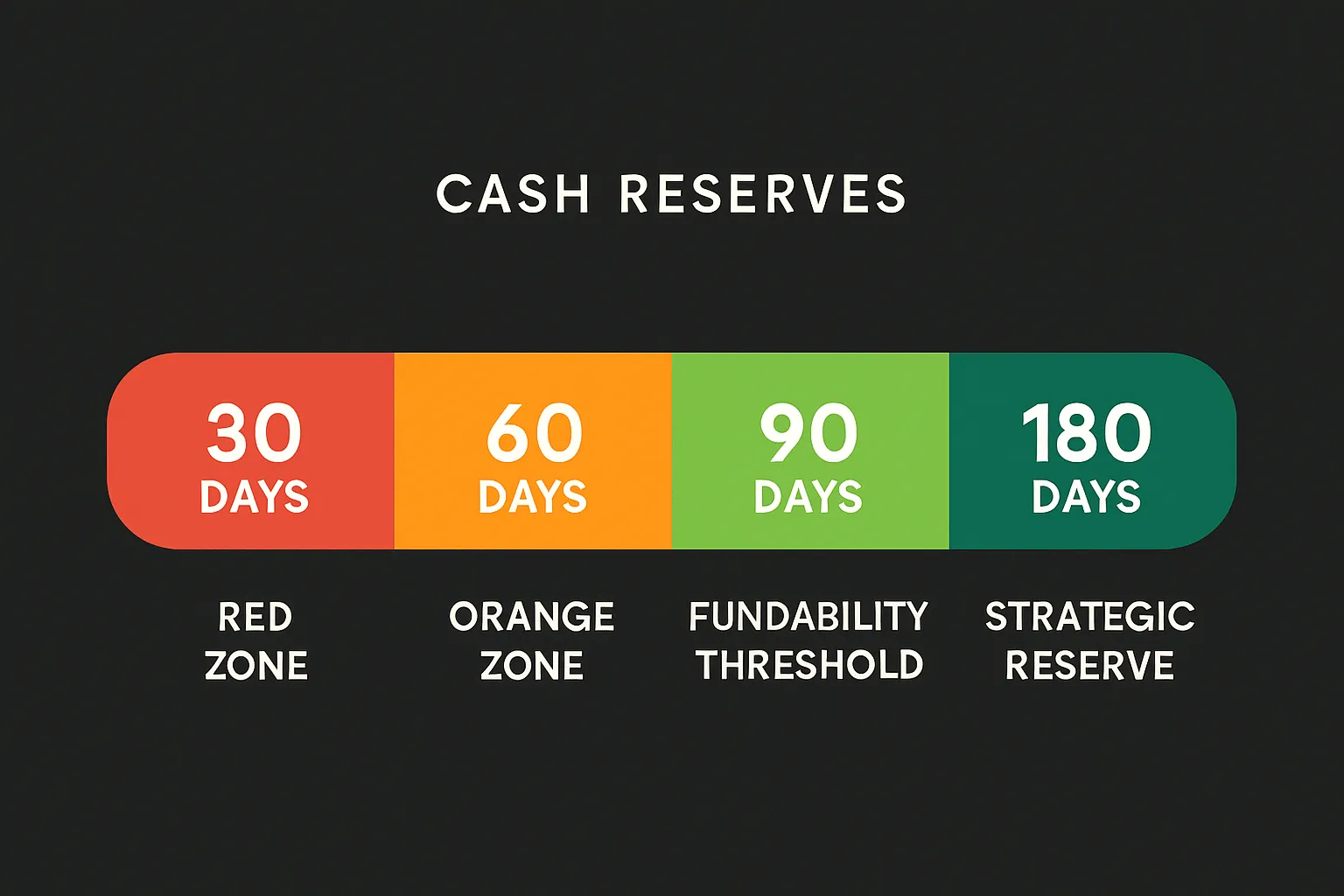

The fundability threshold is 90 days. Below that, you’re a risk. Above that, you’re an asset. The difference in borrowing terms between 30 days and 120 days of runway can be 2–3 percentage points on a loan — which on a $300K loan over 10 years is $50K+ in interest.

The SBA doesn’t publish a hard minimum, but loan officers consistently report that 3 months of post-close operating reserves gives them confidence to approve. Six months makes the conversation easy.

The 30-60-90-180 Framework: Build Incrementally

You don’t need to save six months of expenses next quarter. You build runway in stages, each one unlocking the next:

Stage 1: Zero to 30 Days (The Emergency Fund)

The mechanics:

- Open a separate business savings account (not your operating checking)

- Auto-sweep 2% of every deposit into this account

- On a business doing $30K/month in revenue, that’s $600/month

- In 5 months, you have one month of burn covered (assuming ~$15K monthly burn)

The mindset shift: This money doesn’t exist for operations. It’s not a “slow month” fund. It’s a “catastrophe” fund.

Stage 2: 30 to 60 Days (The Stability Fund)

The mechanics:

- Identify one recurring expense you can eliminate or reduce (that $300/month tool you barely use, the office space you could downsize)

- Redirect the savings into reserves

- Increase auto-sweep to 3–4% of deposits

- Timeline: 3–4 months after Stage 1 complete

The milestone: At 60 days, you can survive your worst month and have breathing room to make decisions instead of reactions.

Stage 3: 60 to 90 Days (The Fundability Threshold)

The mechanics:

- This is where discipline compounds. You’ve now proven to yourself (and your bank statements prove to lenders) that you can accumulate and hold cash.

- Consider routing quarterly tax over-payments into reserves (then pay taxes from reserves — the cash sits longer)

- If you have a line of credit, keep it available but unused. Its existence IS part of your buffer, even if you want cash reserves to be the first line of defense.

The milestone: At 90 days, your next loan application includes the sentence “We maintain three months of operating reserves.” That sentence changes the conversation.

Stage 4: 90 to 180 Days (The Strategic Reserve)

The mechanics:

- Above 90 days, you have optionality. This is where you can start saying no to bad deals, bad clients, and bad capital.

- Consider moving 60–90 day funds into a higher-yield vehicle (business money market or short-term CDs)

- The first 30 days stay in an instantly accessible savings account

The milestone: At 180 days, lenders compete for you. You negotiate from strength. You can push back on terms because you don’t need their money tomorrow.

Realistic timeline: Most businesses with $20K+ monthly revenue can go from <30 days to 90 days in 6–9 months with the auto-sweep plus one eliminated expense approach.

Where to Keep It: Accounts That Work for You

The wrong account erodes your reserve. The right one builds it.

For your first 30 days of runway (instant access):

- Business high-yield savings account (currently 4–5% APY)

- Must be FDIC-insured, no withdrawal restrictions

- Separate from operating checking — out of sight, out of mind

For days 30–90 (accessible within 1–3 days):

- Business money market account (slightly higher yield, check-writing capability for emergencies)

- Sweep accounts that auto-transfer excess daily checking balance into savings

For days 90–180 (accessible within a week):

- 3-month or 6-month business CDs (modestly higher yield)

- Brokerage account with liquid index fund holdings (can be pledged as collateral too)

What NOT to do:

- Keep reserves in your operating checking account (it WILL get spent)

- Lock everything in long-term CDs with early withdrawal penalties

- Put reserves in speculative investments (crypto, individual stocks)

- Mix personal and business reserves (creates tax and legal complications)

Tools like Lendesca can help you track runway alongside other funding readiness metrics, so you know exactly where you stand when it’s time to apply.

The Runway Conversation: Using Your Number in Loan Applications

Once you’ve built 90+ days of runway, use it actively in your loan applications:

On the application itself:

Most loan applications don’t ask for “runway” explicitly. But they ask about cash and liquid assets. Volunteer the framing: “The business maintains $[amount] in operating reserves, equivalent to [X] months of operating expenses.”

In the banker meeting:

Say it out loud: “We maintain four months of operating reserves as a matter of policy.” The word “policy” signals this isn’t accidental — it’s intentional financial discipline.

In your financial statements:

Separate “operating cash” from “reserve cash” on your balance sheet. This shows the lender that not all your cash is spoken for — some of it is specifically earmarked as a cushion.

The compound effect:

- Longer runway → better terms on new loans

- Better terms → lower monthly payments

- Lower payments → more excess cash → longer runway

- Longer runway → stronger negotiating position next time

This is the virtuous cycle that replaces the crisis cycle.

Start Today

Calculate your number right now. Not tomorrow. Open your accounting software or bank statement and do the math:

- What’s your total monthly burn at minimum operations?

- How much accessible cash do you have outside of operating needs?

- Divide #2 by #1.

That’s your runway. If it’s under 30 days, you’re one bad month from a decision you don’t want to make. If it’s under 14 days, you’re already in the danger zone — every day without building reserves is a day closer to the emergency capital trap where expensive money is the only money available.

The good news: building business credit and building runway work together. Every month of demonstrated cash discipline makes you more fundable. Every new credit line (even unused) extends your theoretical buffer.

Ninety days isn’t aspirational. It’s achievable. And it’s the difference between asking for capital from a position of need and asking from a position of strength.